- News

- Investing

On 23 June 2016 the UK voted in a referendum to leave the European Union, by a narrow margin of 52% to 48%. The UK had been a member state of the EU since 1973 and the outcome of the vote – and the decision to abide by what was a legally non-binding referendum – caused widespread anger among ‘remainers’ and jubilation among ‘leavers’.

While the fierceness of the debate may have dialled down over the past 10 years, Brexit still invokes strong feelings in many of us. But what material impact has leaving the EU had on household finances, stock markets and even (arguably) the Eurovision song contest?

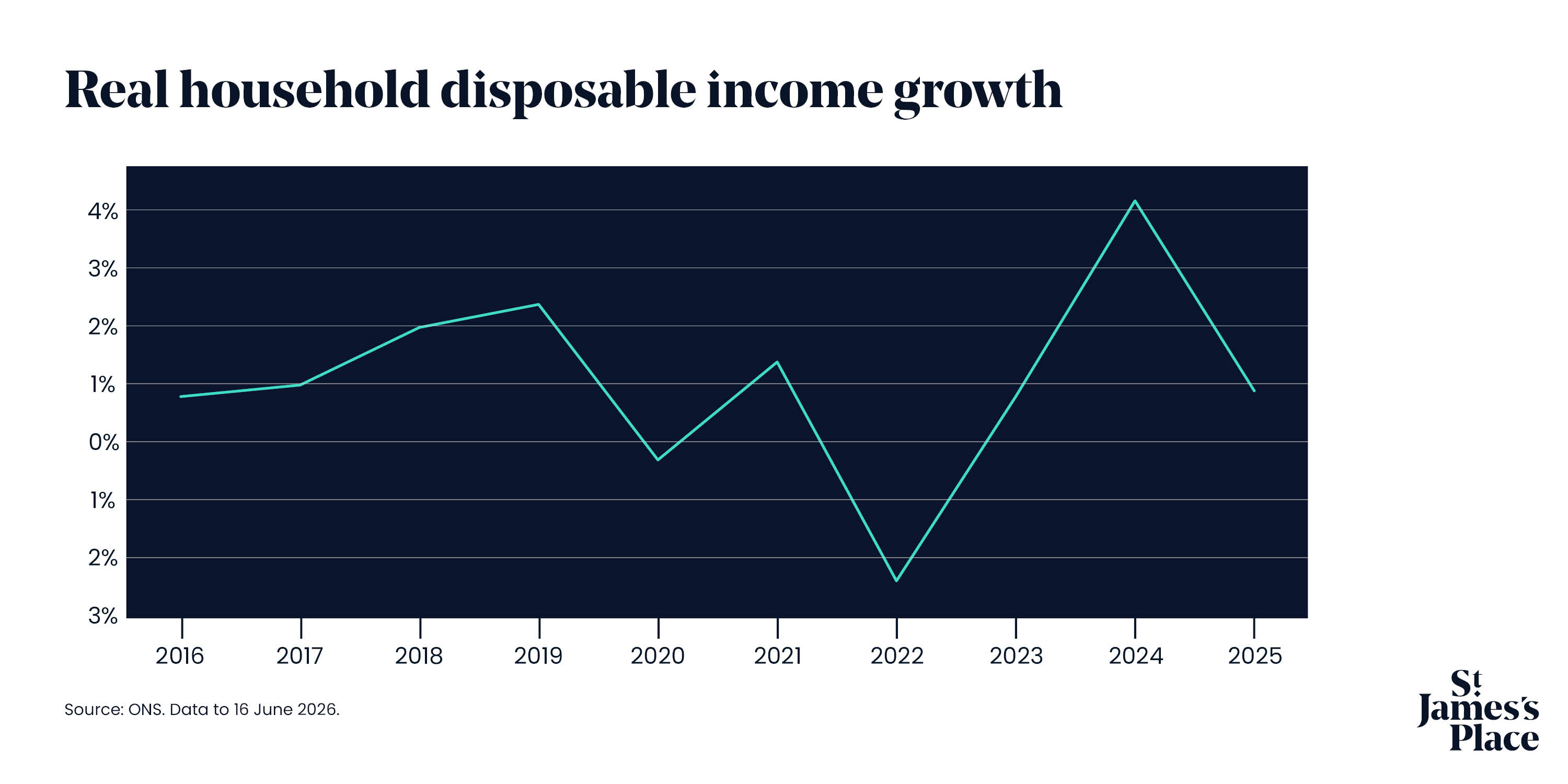

Household finances under pressure

Over the past decade, UK household finances have felt increasingly strained. Until 2019, disposable income grew slowly but steadily. But since the pandemic in 2020, the picture has become far more unpredictable, shaped by events such as the Russia-Ukraine conflict and, more recently, global trade tensions and conflict in the Middle East.

The result has been sharp swings in household finances rather than sustained, reliable growth. For many households, this has translated into a clear sense that wages have struggled to keep pace with the rising cost of living in recent years.

FTSE 350 vs STOXX 600 – how markets compare

The FTSE 350 is a useful index for looking at the strength of the British economy. While the FTSE 100 is more well known, its international diversification means most of its sales and profits are generated abroad, and therefore it can be affected by downturns elsewhere. In contrast, the FTSE 350 adds smaller but more domestically focused companies.

Comparing its performance to the European STOXX 600, there have been key differences since Covid. While the FTSE 350 lacked the explosive post-pandemic bounce back of other markets, it also avoided the worst of the 2022 drop. Since then, UK shares have underperformed their European Union (EU) counterparts, although they also experienced less volatility when President Trump’s Liberation Day tariff announcements sent global equity markets lower. It’s worth noting there are other factors that may have impacted returns – such as sector makeup.

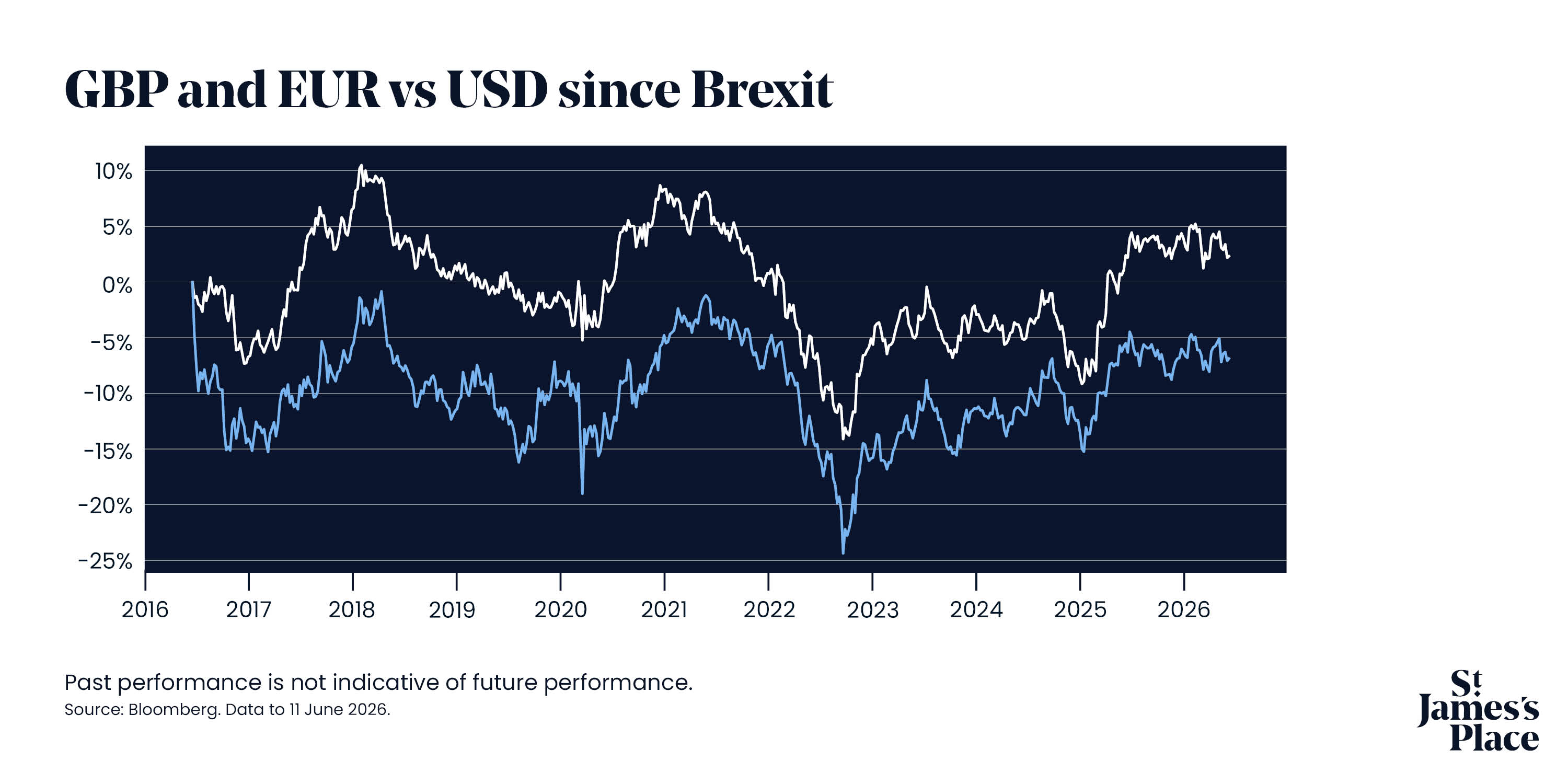

Sterling, the euro and the US dollar - a higher risk premium for UK assets

The UK decision to leave the EU raised the risk premium on UK assets. Despite occasional cyclical rallies, the pound has not been able to break convincingly with its post-referendum malaise. Brexit altered expectations for the UK’s growth outlook, with investors reassessing the outlook for productivity and competitiveness. Weaker and more volatile capital inflows, set against structurally larger current account deficits, left the currency more exposed to shifting investor sentiment as the Brexit negotiations dragged on.

The pound fell victim to self-inflicted wounds such as the Truss mini-budget in September 2022. External shocks also played a part. These included the post-Covid inflation surge as well as the energy price hike following the invasion of Ukraine, and the more recent strikes on Iran.

Against the dollar, the euro has performed notably better than the pound over the same period. It outperformed relative to the dollar, notably during 2017/8 thanks to healthy regional growth and the dollar’s weakness during 2017. While there has inevitably been some cyclicality in the euro over the decade, this has reflected specific, temporary factors, rather than the structural repricing experienced by the pound.

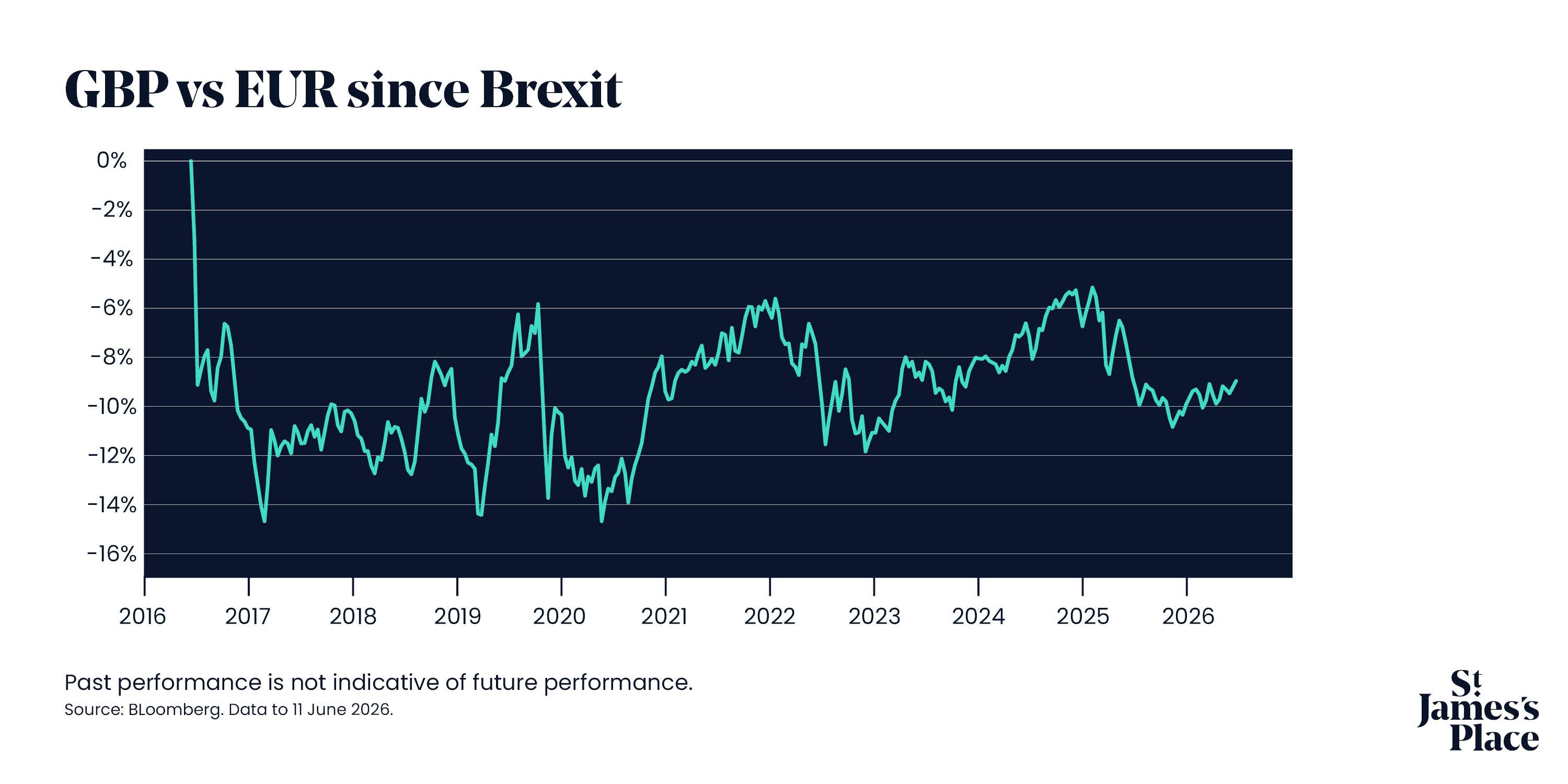

Pound struggles against the euro

While the GBP/USD and EUR/USD can show up periods of broader dollar strength, it is the GBP/EUR rate may offer a more helpful gauge of relative performance between the UK and eurozone. While the euro is a global reserve currency, it doesn’t have the size or relative appeal of the dollar. This means that the GBP/EUR is more useful at capturing the dynamics between these closest of trading partners. The eurozone is also the UK’s single most important market.

The chart paints a bleak picture of the pound’s performance against the euro, reflecting a sharper deterioration with few signs of a meaningful recovery. There was a partial rebound for sterling in the immediate post-Covid period. Higher inflation led the Bank of England to do so following the pandemic. Yet the costs to the economy following spikes in inflation resulting from the invasion of Ukraine, and more recently the Iran war, have kept a lid on any sustained recovery in the value of the pound.

The UK’s weak economic growth, its need for imported energy and domestic political instability are preventing the pound from closing the gap on a sustained basis.

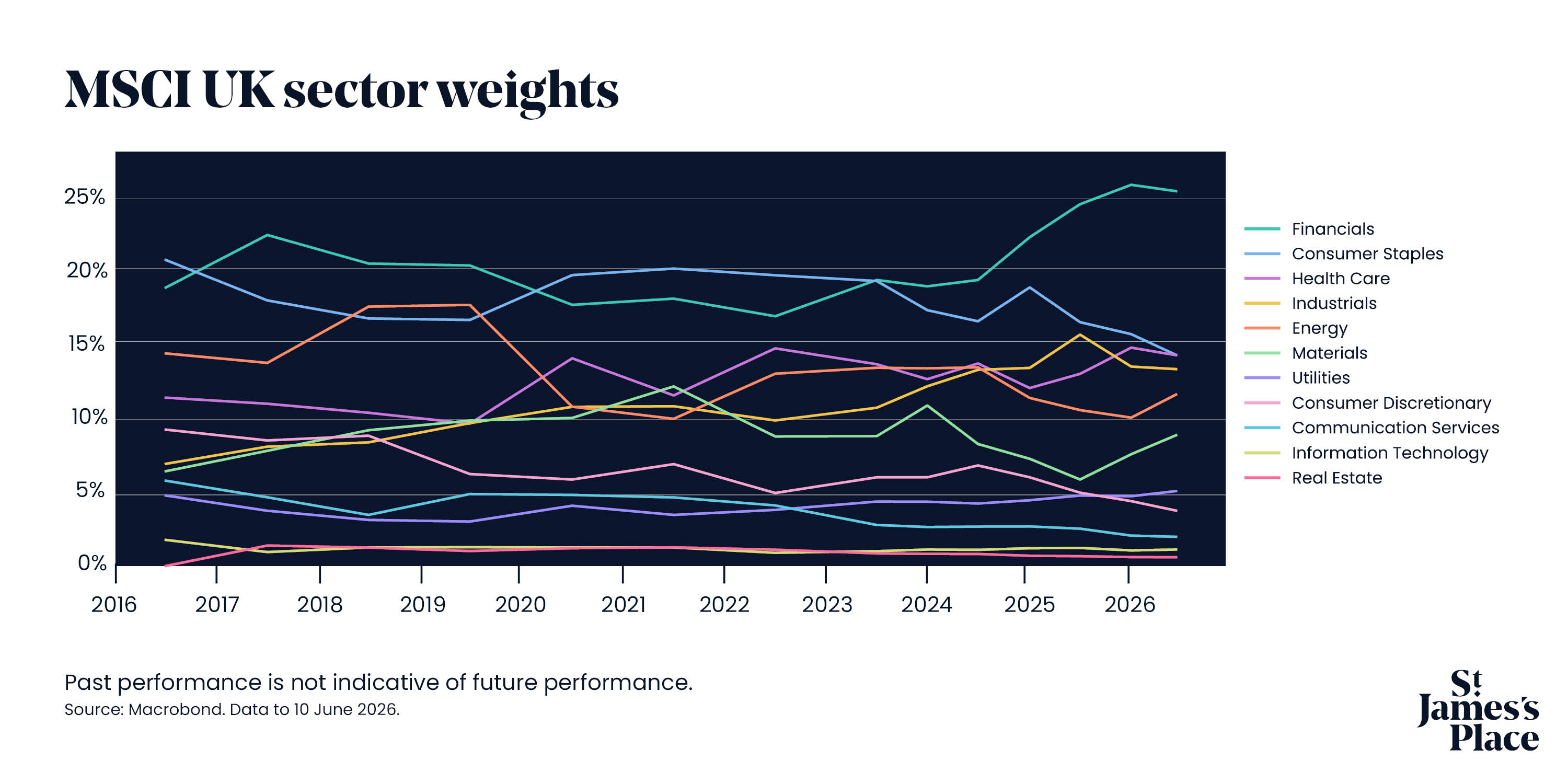

UK stock market sector changes – trying to keep up, but is it enough?

There have been some significant sector changes in the UK equity market in the decade since the referendum. The MSCI UK index, which accounts for 85% of the UK equity market (excluding small and less liquid companies) is regarded as a good proxy for the UK economy.

Financials are now the largest segment, accounting for a quarter of the total index. This sector is regarded as a leading indicator, outperforming as investors anticipate a pick-up in the economy, such as following the pandemic. Further drivers are higher net interest margins as interest rates rise, and a broad financial re-rating as investor optimism improves.

In contrast, the UK’s weakness in quoted tech companies marks a sharp contrast with the US and, increasingly, Europe. Combined with the shrinkage in communication services, this emphasises the UK’s limited exposure to high growth and high valuation sectors/companies. It is these sectors that are expected to drive investor appetite and market returns.

Consumer staples, that is companies providing goods that people need irrespective of the state of the economy or their personal circumstances (also known as defensives) have lessened in importance over the decade. Weaker growth and the rotation away from defensive companies with undermanding valuations have also diminished their relative importance.

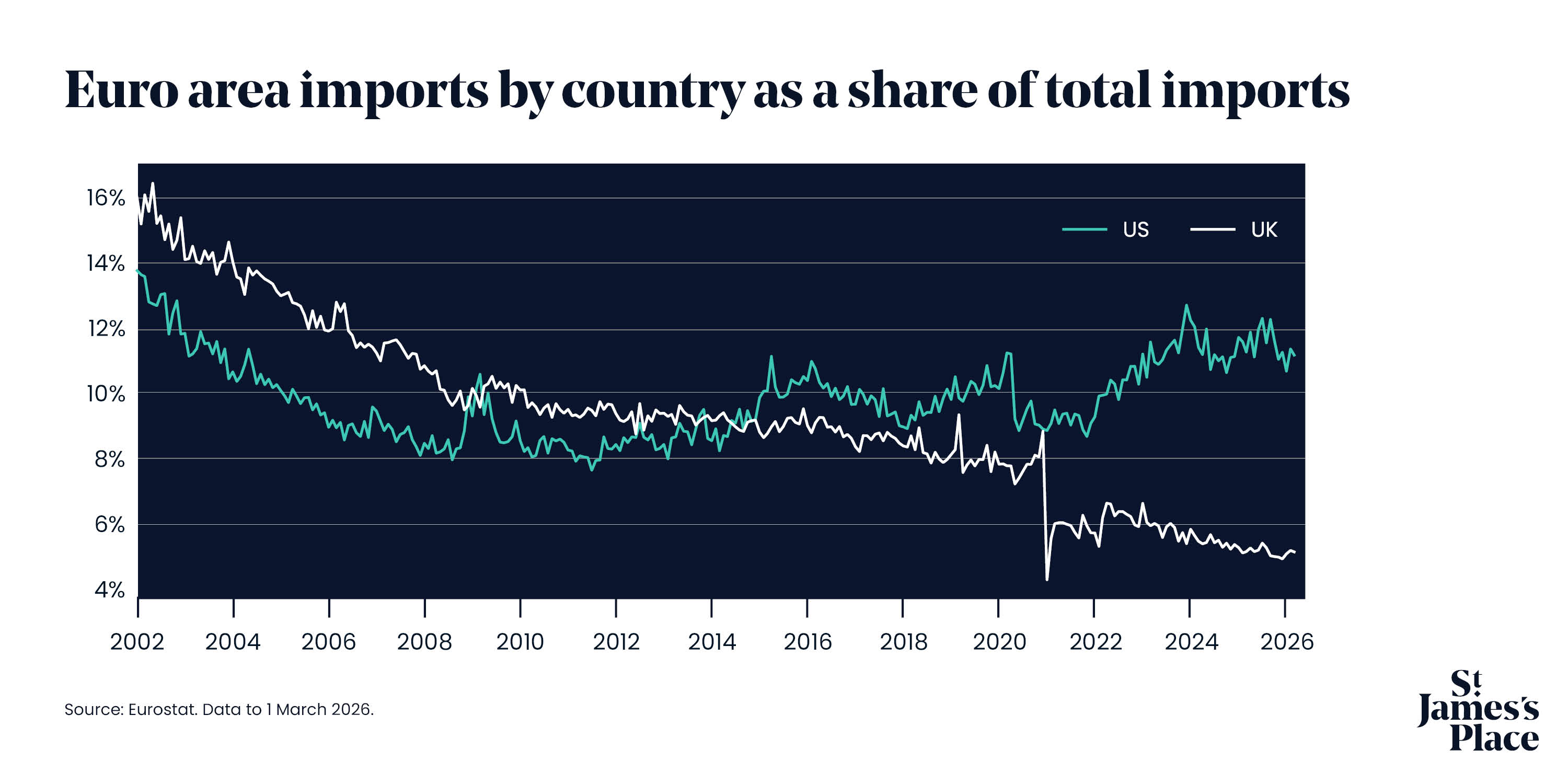

The importance of imports

British exports to the EU have been gradually declining since the start of the millennium, with other markets taking a greater market share. While the trend existed before Brexit, there was a noticeable drop off at the start of 2021 when the UK formally left the EU single market, as the chart below shows.

Despite a slight recovery in the year that followed, it has since returned to its downward trend. The United Stats has been a notable winner from the trade friction between the EU and UK. Even after Trump’s tariffs added extra headaches to EU-US trade, US imports remain well above where they were pre-2021.

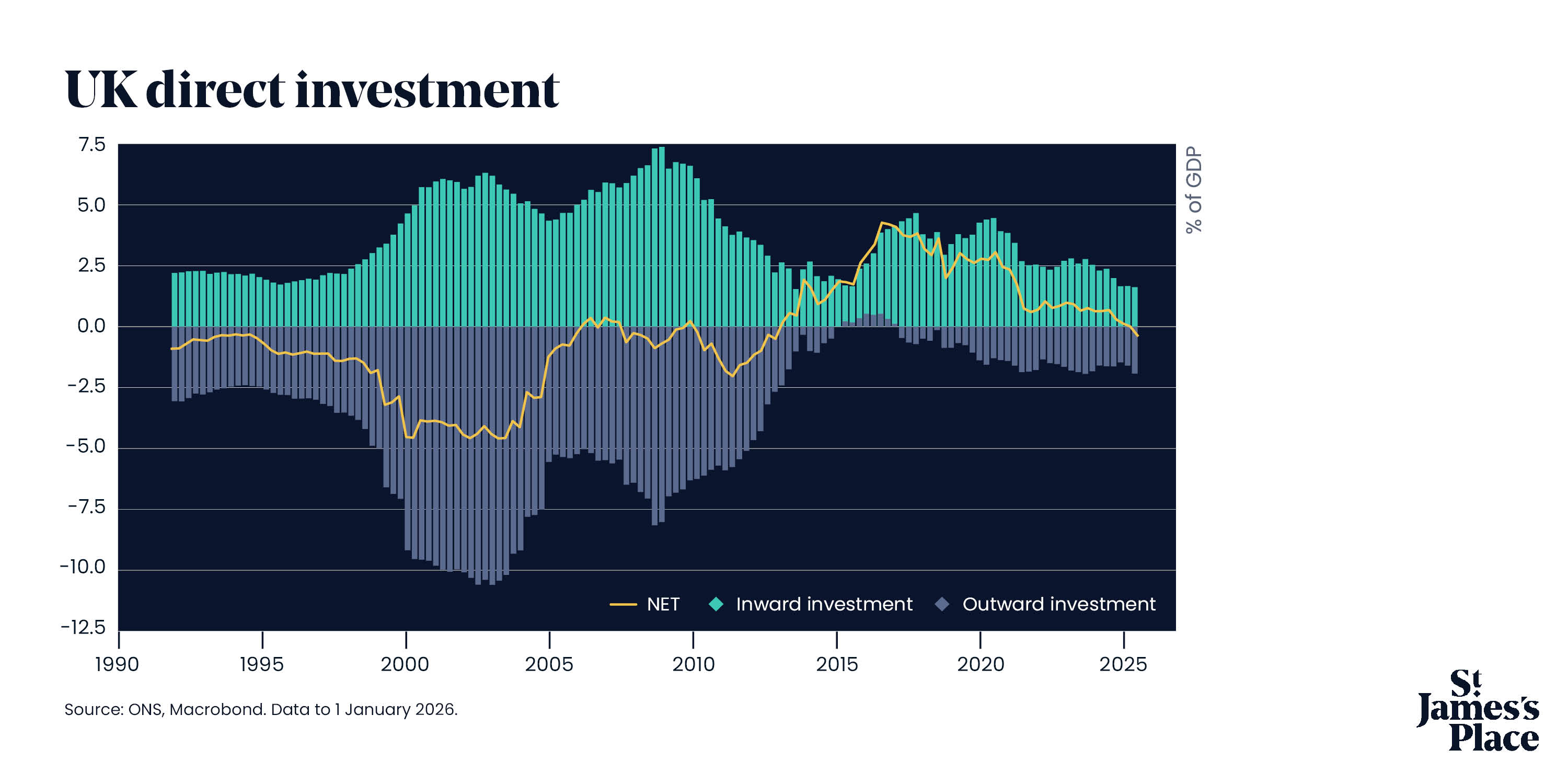

Foreign direct investment – a downward trend

The clear trend since 2016 has been a drop in direct investment both into and from the UK. Outward investment collapsed among the uncertainty of the immediate aftermath of the Brexit vote. Although it has slightly recovered since, it remains well below pre-Brexit levels.

There was also a drop in inward investments in 2016, however not to the same extent as outward. As a result, UK direct investment went from net outward to net inward.

Although last year that position reversed, that was more down to inward investment continuing to decline than any improvement in outward investment numbers.

Investment in sectors such as automotive manufacturing and aerospace have been especially hard hit in this period, with several Japanese carmakers either pausing expansion plans or even closing plants.

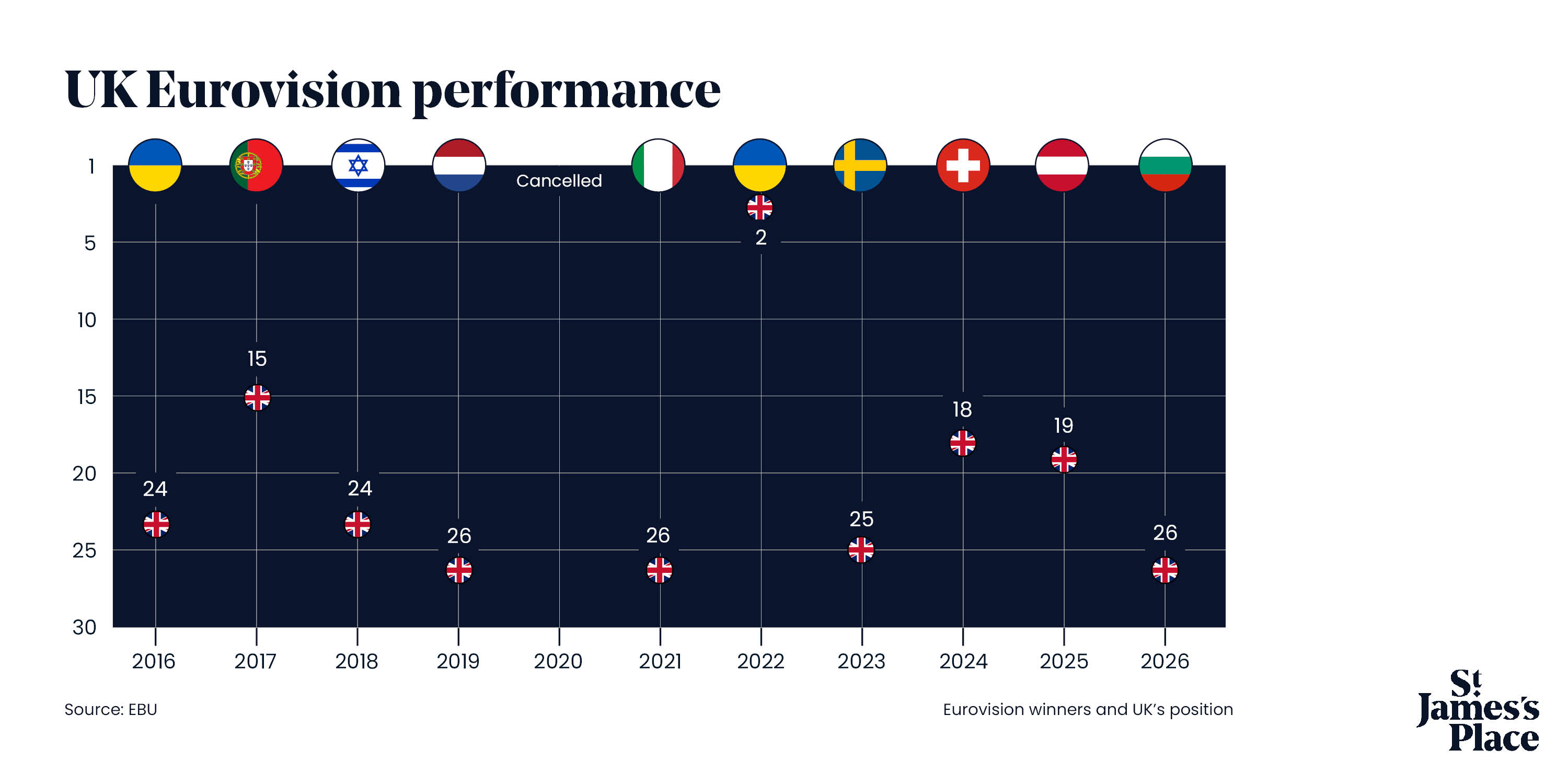

Eurovision – how the mood music has changed since Brexit

While the Eurovision song contest is entirely unconnected to markets, the performance of different countries including the UK is often thought to be closely linked to the political backdrop of the time.

Overall, the UK has come second more times than any other nation, finishing as runner up 16 times in its 69-year history. Yet since Brexit, the UK appears to have been on a downward trend in terms of popularity.

In the first year following Brexit, the UK came 24th out of 26 nations with a dismal 62 points. Commentators at the time suggested the decision to leave the EU led to negative voting against the UK. 2021 was an even more dismal year, with nil points scored by the UK. Were voters still scarred by Brexit or was it just a terrible song?

As the above chart shows, aside from a rare second place in 2022, since 2016, the UK has placed no higher than 15 out of 26 nations. In 2022, the winning country was Ukraine. It followed the Russian invasion of Ukraine earlier that year and huge support across the UK and Europe for the beleaguered country.

The UK has been in the bottom three in six out of the ten years. Song contest or political popularity contest? It is not always easy to tell.

Most popular articles

Most recent articles