- Investing

After years of underperformance, smaller companies, known as small caps, had a stellar start to the year. Yet with values still relatively low, could it be worth investors taking a closer look?

At a glance

- Years of weak performance mean smaller company value low compared to large companies.

- The sector offers a potential diversifier within a portfolio.

- However, smaller companies are inherently riskier than larger companies.

In recent years, it has sometimes been hard to escape talk of the Magnificent 7 – the group of seven of the world’s largest and most influential companies which includes the likes of Apple, Amazon and Nvidia. These companies have played a major role in driving stock market returns in recent years. Even when their performance ebbs somewhat, other tech giants, defence companies or similar have naturally filled the news cycle. But by only looking at the biggest companies out there, are we ignoring the vast world of smaller companies (small caps)?

From small to not-so small

The name ‘small cap’ is often something of a misnomer. While these companies will barely register as a blip on the radar next to the giants of the FTSE 100 or S&P 500, they can be quite large.

There is no hard and fast threshold for the sector, but generally companies valued at between £300 million and £2 billion are classed as small cap. In the US, it’s US$300 million to US$2 billion – so broadly comparable, once currencies are considered.

At this size and scale, many household names will fall into the small cap sector. In the UK, fast food chain Greggs is considered a small cap, despite being ubiquitous on the high street. Meanwhile US brands such as Crocs and GoPro have international footprints yet are still technically in the small caps space.

From small beginnings to larger outcomes

Games Workshop, a British manufacturer of miniature wargames, provides an interesting example of why this sector could be attractive to investors.

The company (creators of the Warhammer and Warhammer 40k IPs, among other things) has spent most of its history firmly in the small cap space, or below, with a market capitalisation of just under £300 million in 2016. However, over the past decade it has witnessed explosive growth. The value of the company (the market cap) quadrupled in 2017, and it entered the FTSE 100 in 2024. Games Workshop is now worth £6.7 billion at the time of writing. £500 invested in 2016 would now be worth over £20,000.

Clearly this is an outlier, and most small caps will never achieve this level of growth, and many will fail. But it highlights the fact that sales and earnings can grow very rapidly from a low base at small companies and share prices will respond.

An active touch

While small companies have more room to grow in theory, they are also more likely to fail. AIM listed companies like baker Patisserie Valerie and insurance claims and technology group Quindell are two well-known examples of small caps that collapsed thanks to accounting issues.

Being smaller, they typically have less access to cheap capital than larger companies, which can mean fewer reserves to draw on in tough times.

They also tend to be less diversified, relying on fewer products or markets, meaning a single business line struggling could prove harder to absorb than for larger businesses.

However, this is one of the reasons specialist active managers should be able to provide significant value in this space - they can, in theory, spot risks and issues early (though there is no guarantee they will get it right).

The potential risks are compounded by a lack of analyst coverage of the market. This makes mispricing more likely within smaller companies, meaning their share price doesn’t always reflect their true value.

Partnering with an expert means finding a manager that looks to take advantage of some of these mispricings, and attempts generate higher returns than a passive strategy. Passive or whole market strategies won’t be able to distinguish between struggling companies and those that offer potential opportunities.

Even with the potential benefits active management can bring, it is impossible to escape the fact that investing in small caps is more risky than larger companies. Smaller companies are more likely to fail than larger companies as discussed above, and the sector is inherently more volatile, meaning investors could lose money, particularly over shorter periods. It is also worth noting that shares in smaller companies are generally less liquid than for larger companies, meaning in some instances they might be harder to buy and sell. Investors should be prepared to lose some or all of their investment.

For investors with a low risk tolerance, this might mean the sector is not appropriate.

However, for those with an appropriate risk tolerance, small caps offer a potential diversifier compared to other equities. Small caps do not move totally in sync with large caps for many reasons. In general, smaller companies derive a much higher proportion of their income domestically than large companies do. Smaller companies can fill different niches and are generally more susceptible to changing economic conditions than larger companies (meaning their share prices can be more reactive).

Much of the top end of the market is currently facing concentration issues. A tiny number of the largest few companies are dominating the overall market like never before. Right now, the performance of the S&P 500 remains largely anchored on sentiment around AI. If opinions turn sour, that is enough to move the whole market lower (as seen in early 2026).

While small caps have plenty of companies that are related to the AI supply chain, or stand to benefit from it, the sector also features swathes of companies who have little to no exposure to AI.

Past performance is no guarantee

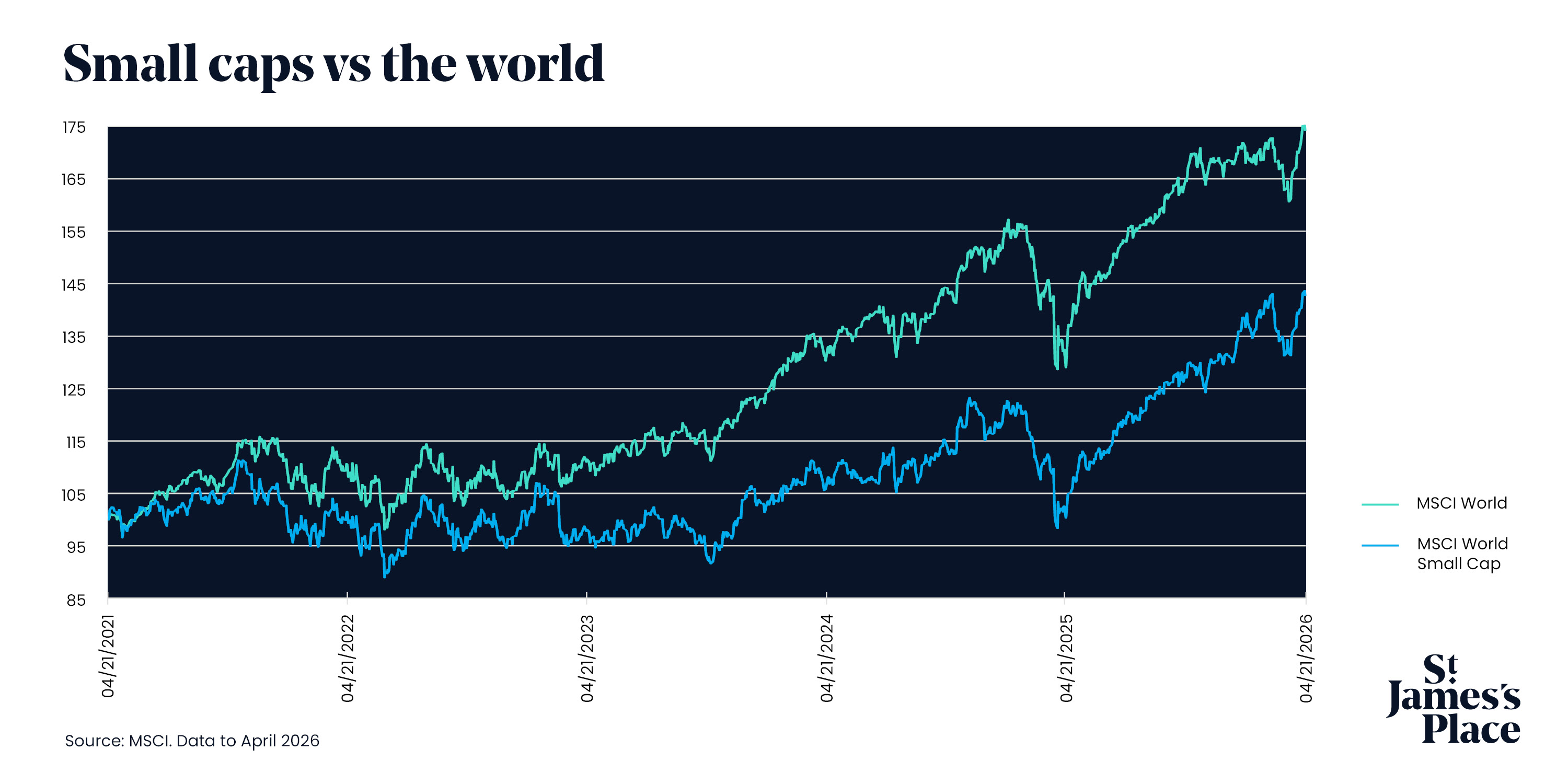

Despite this, it’s hard to argue that recent years have not been more favourable for giant companies. In recent years, indices for large companies have generally outperformed those for smaller companies with reasonable consistency. This makes the case for small caps a difficult one to make – why take greater risks for lower returns?

However, this has also opened something of an opportunity. The small cap sector is currently trading at a historic discount compared to larger companies. Markets never remain static, they ebb and flow, and today’s winners can become tomorrow’s laggards. If small caps values were to begin to revert to historical norms relative to their larger peers, this could offer patient investors an opportunity.

The first quarter of the year showed some evidence that the trend had started to reverse. For example, over the first four months of the year, the S&P SmallCap 600 outpaced the S&P 500 by 8.5%.

Even with this recent outperformance, small caps valuations appear cheap compared to the wider market, though this may reflect higher risk. Given the ongoing concentration issues at the top end of the market, small caps may well play an important role in the coming years for well-diversified portfolios.

Source: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2025. FTSE Russell is a trading name of certain of the LSE Group companies, FTSE is a trademark of the relevant LSE Group companies and is/are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

© S&P Dow Jones LLC 2026; all rights reserved.

Most popular articles

Most recent articles