- News

- Investing

The Bank of England (BoE) held the base rate at 3.75% this week.

But market expectations are now that the base rate will rise during 2026. This is because inflation is likely to go up due to increased oil prices caused by the prolonged conflict in Iran. The Bank of England uses interest rates as a tool to control rising inflation.

Mortgages are closely related to the Bank’s base rate, so what does this mean for anyone looking to buy or remortgage a property and in need of a new mortgage deal? Would a fixed or a tracker rate mortgage offer better value over time?

Here we explore the advantages and downsides of both mortgage types to help you with your decision.

At a glance

- Fixed rates appeal to buyers who need the certainty of knowing what they will be paying every month.

- The rate on a tracker mortgage is directly linked to any changes in the Bank of England base rate. This means the mortgage rate may go up and down during the term.

- Comparing multiple lenders and deals and acting early can improve your chances of accessing a competitive mortgage rate.

Fixed rate mortgages

With the Iran conflict showing no signs of ending, economists are anticipating the Bank of England will soon increase the benchmark base rate to tackle rising inflation. As a result, lenders have been putting up their fixed mortgage rates.

While yet to feed through fully, the increased cost of oil due to the Iran conflict and the disruption to shipping from the closure of the Strait of Hormuz are widely expected to lead to a spike in inflation in the coming months.

In such environments, central banks tend to keep borrowing costs higher to control rising inflation.

Analysts believe the BoE may increase the base rate at least twice, if not three times over the next year.

For borrowers with concerns about rising rates, a fixed rate mortgage offers peace of mind that payments will not change during the term of the deal. It is the main reason why most mortgage borrowers choose fixed rate deals over tracker rates.

Features of fixed rate mortgages:

- Short-term fixed rates tend to be the most competitive, with borrowers paying a premium to fix their mortgage rate for longer, such as five years. But this is not always the case.

- The cheapest fixed rate deals will often have high arrangement fees. That is why it is important to work out the total cost of the deal.

The certainty that comes with fixed rate mortgages tends to have a cost, however. Deals often include high early repayment charges if you want to repay the mortgage or switch to another deal during the fixed rate term. This can mean less flexibility compared to other types of mortgage.

Tracker mortgages

Tracker mortgages are typically linked to the BoE base rate, with a lender’s margin added on top. For example, a typical deal might be set at BoE base rate (currently 3.75%) plus 0.5%, giving a mortgage rate of 4.25%.

However, the mortgage rate will then reflect any changes to the BoE base rate during the term of the deal. If the base rate goes up, so does the rate on the tracker mortgage. If the base rate falls, so will the rate on the mortgage.

This means homeowners with tracker mortgages are more exposed to changes in economic conditions, such as rising inflation which tends to lead to increased interest rates.

As a result, budgeting can be more challenging for such borrowers compared to those on fixed rate deals.

Tracker rates can be taken out over periods of two years, three years, five years or even longer. Some lenders offer a lifetime tracker, which means the deal you sign up to you can keep for the life of your mortgage. However, these tend to be less competitive on rate.

Features of a tracker rate mortgage:

- Buyers benefit from lower rates if interest rates fall.

- There is greater transparency, as the mortgage rate is linked to the BoE base rate.

- Some tracker deals have no early repayment charges or lower charges compared to those applied on fixed rate deals. This allows borrowers to overpay or switch deals with greater flexibility.

It is worth noting, however, that switching from a tracker to a fixed rate deal once interest rates have started to rise may mean locking in at higher rates than those available today.

Rates during economic stress

So, what is the best way to pick a mortgage deal?

Periods of economic instability often lead to quick changes in mortgage pricing, with deals and rates changing daily. Waiting days or weeks – to find a deal can make a huge difference to what borrowers end up paying on their mortgage.

This can make a significant difference in cost over the life of the mortgage deal, which might be two, three, five or 10 years, for example.

Fixed rate deals in particular tend to have a shorter shelf life in volatile periods, as lenders withdraw products and reprice them to reflect market expectations.

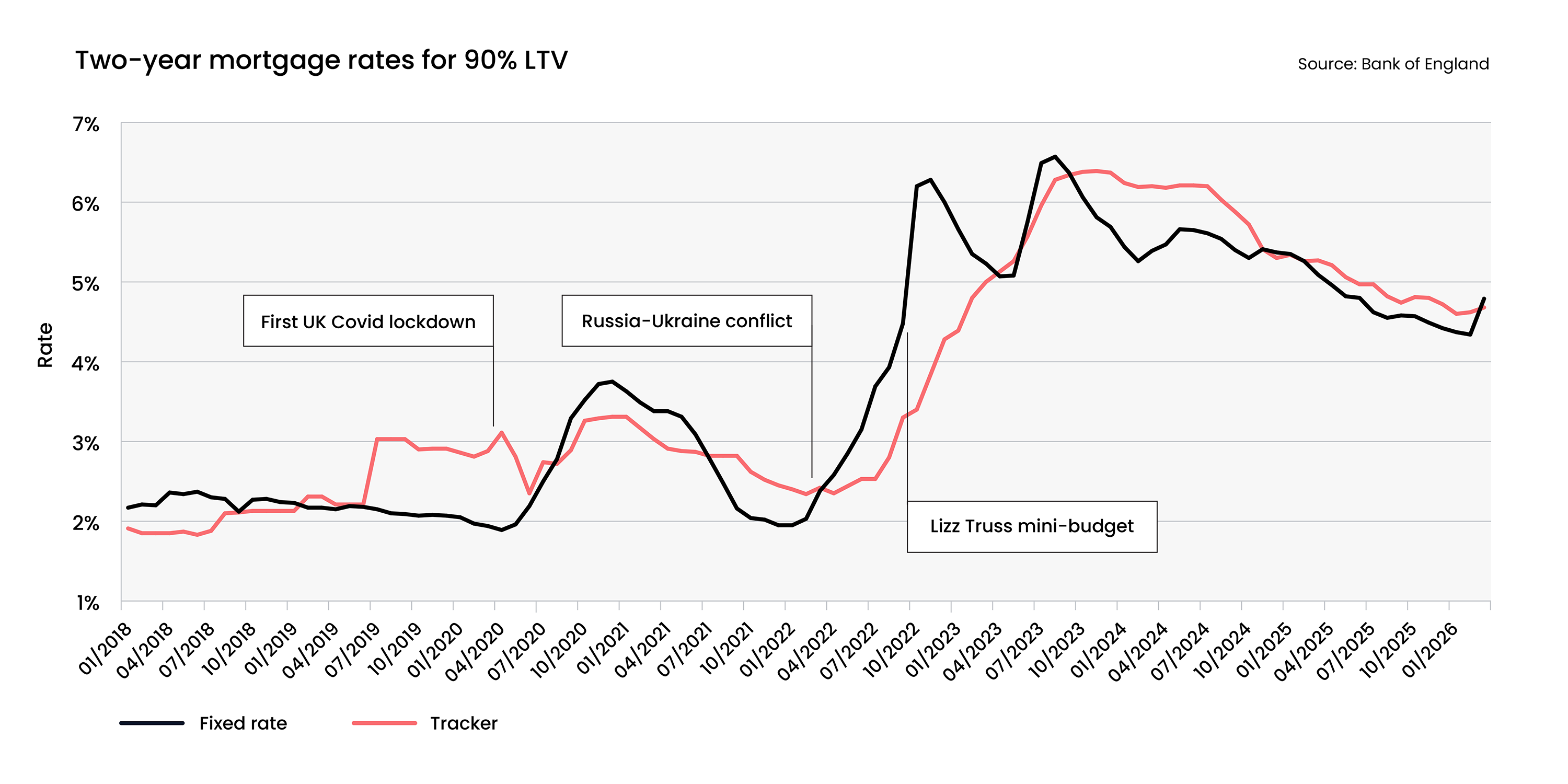

Source: Bank of England – April 2026.

This was evident in February 2022, when rising energy prices drove up inflation for a sustained period following the outbreak of the Russia-Ukraine conflict.

As the chart above illustrates, the average mortgage deal available to buyers at the time was 2.03%. This was for buyers with at least 10% deposit or equity in their property (90% loan to value or LTV). But only four months later, the average deal price at 90% LTV had risen to 3.15%.

Borrowers on equivalent 90% LTV tracker deals were paying an average rate of 2.34% in February 2022. But this had risen to 2.53% by June.

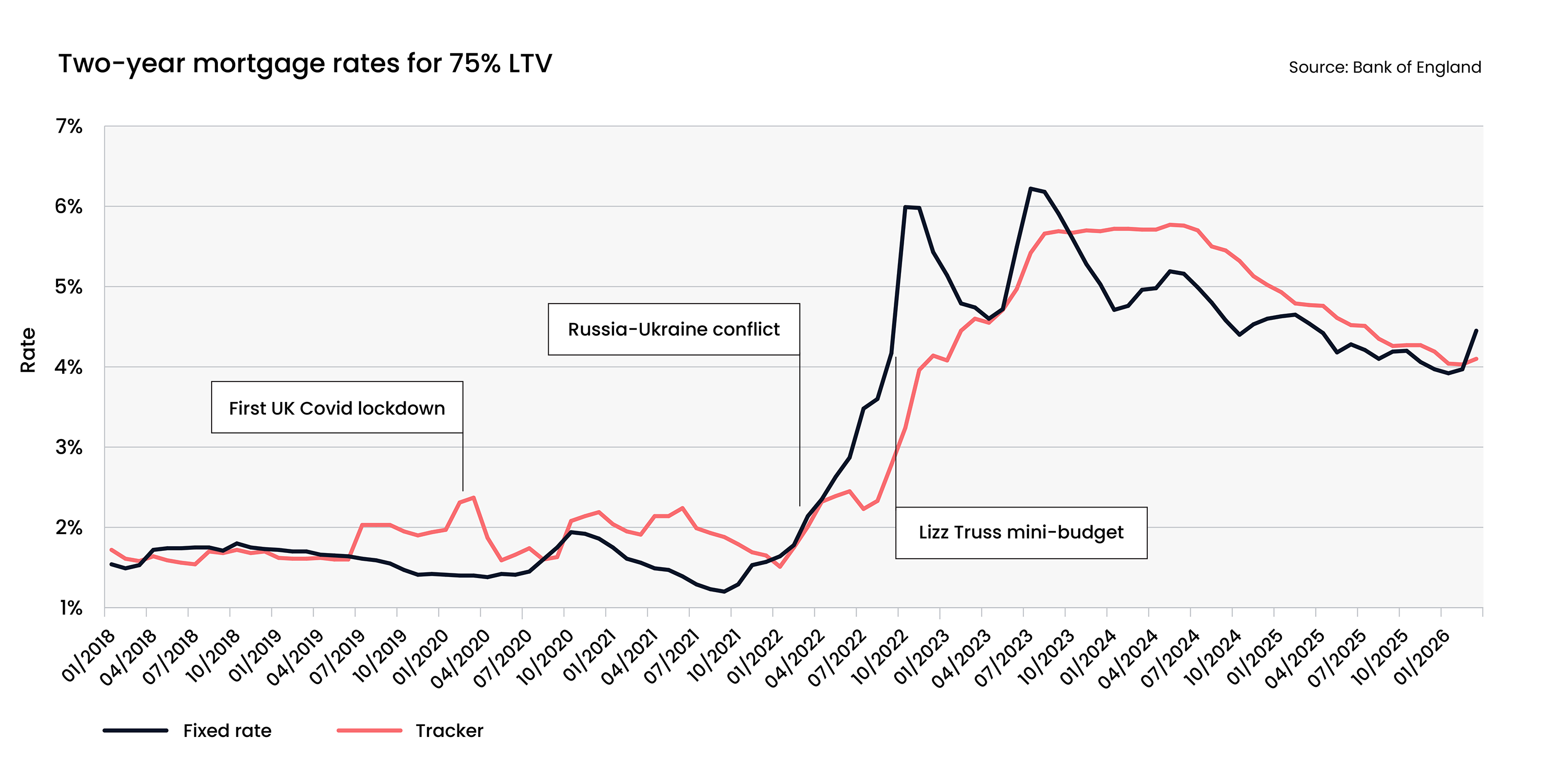

Source: Bank of England – April 2026.

A two-year fixed rate deal at 75% LTV cost an average of 1.78% in February 2022. But by June this had increased to 2.87%.

Equally, tracker borrowers at 75% LTV were paying an average 1.75% in February 2022, but this had risen to 2.45% by June the same year.

Short or long-term deals?

Choosing the term of your mortgage deal will come down to your financial situation and preference. Fixing for longer, such as five years, can give long-term peace of mind that you know exactly what your budget will be. This can help with financial planning. But you will not benefit during that time if interest rates fall.

Opting for a two-year fixed rate might give the lowest starting pay rate on your mortgage, but the fees can be high on the best deals – typically between £1,000 and £2,000, for example. In addition, you will need to remortgage, potentially paying another high arrangement fee, in two years.

Short-term tracker rates tend to have more competitive rates, compared to longer-term or lifetime tracker deals. But long-term tracker rates often come with greater flexibility, such as the opportunity to repay the loan in full without penalty, which may suit some borrowers.

Choosing the best rate for you

Buying property or remortgaging is rarely straightforward and selecting the right mortgage deal can feel tricky. Volatile economic conditions only add to the pressure.

Even though the Iran conflict has pushed mortgage prices up, there are steps buyers can take to improve their chances of a better deal. These include:

- Start researching up to six months before an existing deal ends. Many lenders will allow you to secure a new deal up to six months in advance.

- Compare multiple lenders and consult with a mortgage broker, who may have access to exclusive deals.

- Be prepared to switch products if a more competitive deal emerges before completion.

- Review your LTV, as moving into a lower LTV can unlock better rates. There are many ways to achieve this, such as saving more or for longer, or overpaying your mortgage.

- Look beyond headline rates and consider the total cost of a mortgage deal, including any product fees, early repayment charges and incentives.

- Seek specialist advice from a mortgage broker for more complex borrowing needs.

For many people, property is the largest financial commitment they will make. Finding a mortgage can be stressful, so having trusted support through the process could make a big difference.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Most popular articles

Most recent articles