- News

The recent attacks on the Iranian leadership and subsequent retaliatory actions across the Middle East have caused widespread geopolitical volatility. Unsurprisingly, they have also left many investors wondering what actions they should now be considering.

At a glance

- The latest attacks on Iran and its retaliatory strikes across the region led to a sell-off in global markets.

- While still volatile, many assets have since rebounded off their recent lows.

- History shows that stock markets recover after such shocks and the best outcome to maximise eventual returns is to remain invested.

This appears to be the start of an open-ended war in one of the most geopolitically sensitive areas of the globe. The availability of 24-hour news makes it easy to monitor, almost in real time, what is happening.

Despite this information flow, perhaps one of the only certainties is the uncertainty about what will happen. At the beginning of this week, investors

responded to the attacks on Iran in a similar way to their response to Russia’s invasion of Ukraine four years earlier. Stock markets fell, while traditional “safe haven” assets such as the US dollar and US treasuries rose.

In this situation, Iran’s ability to control the Strait of Hormuz means it can influence the global economy. Approximately 20% of the world’s oil and 90% of the oil destined for Asian markets passes through the straits. Many investors are therefore understandably concerned about what restricted energy supplies will do to the global economy.

Taking a breath – what market history shows us

Many investors will be feeling the stress and uncertainty associated with the current events. However, those tempted to reduce their holdings should remember that market history, led by the US, shows us that following geopolitical shocks, stock markets bounce back.

For example, in the days following Russia’s invasion of Ukraine, the US S&P 500 fell by more than 7%. During the first two weeks, oil prices rose by 40%. Natural gas prices climbed 180% according to the European Central Bank. Yet four years on, with the conflict still ongoing, both the US and European stock markets (the latter severely affected at the time by the halt to Russian energy supplies) remain within touching distance of their all-time highs. Meanwhile the oil price remains well below the levels of four years ago. This is despite the double-digit percentage price rise per barrel seen over the past week.

Likewise, many key global indices including the S&P 500, the FTSE 100 and China’s Shanghai Composite were off their recent lows.

The same is true of the Cboe Volatility Index, known as the “Fear index”. While this rose initially, l reflecting more concerns in the market, it too has subsequently eased. It is now well under the level associated with high levels of fear in the financial markets.

The reaction in bond markets has been more nuanced. While initially the flight to safety pushed bond prices higher (and bond yields lower), concerns about the effects of higher energy prices on inflation led to a reversal of this position. US Treasury yields are now higher than they were just prior to the US action.

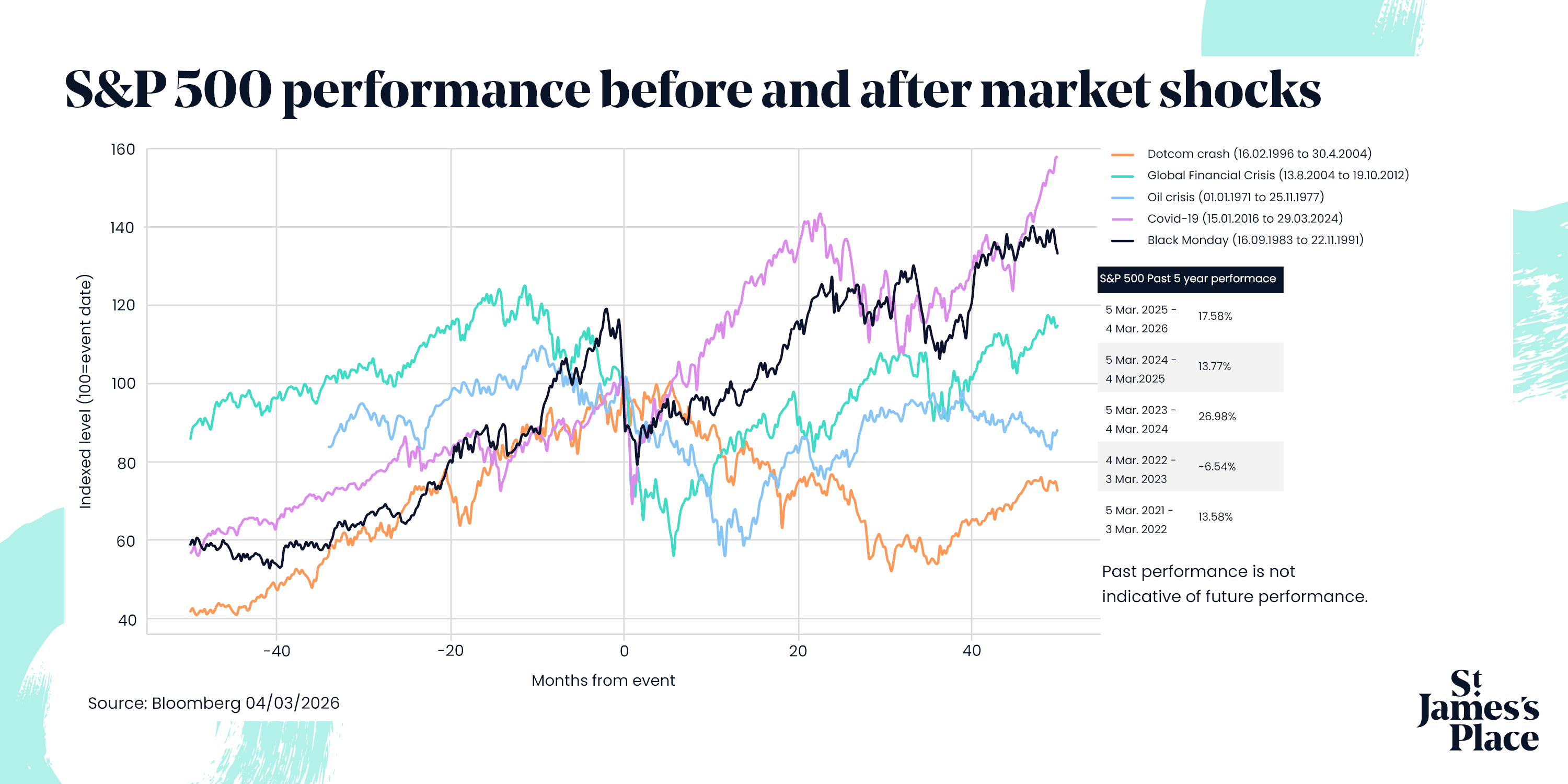

As Joe Wiggins, Investment Research Director at SJP points out, times of stress and uncertainty are the worst time to make investment decisions. This is because our instinct is to anticipate a worst-case scenario coming to pass. Selling out at these levels will often see investors missing out on the subsequent recovery. This is shown in the accompanying chart of the S&P 500’s performance during major market shocks. Over the longer term and in the majority of cases, the benchmark has rebounded within months of the start of the event.

Joe urges investors to apply the same discipline when markets are falling as when they are rising and the newsflow is calm. He recommends investors consider the questions on the below checklist. before being tempted to take any action.

- Do I have confidence in predicting the outcome of the current situation?

Predicting the developments of these highly complex situations is an impossible task. Fortunately you are not required to do so to deliver strong long-term investment returns.

- Can I reliably anticipate the financial market implications?

If predicting how geopolitical events will unfold is difficult, predicting how financial markets will react might be even more difficult. It requires knowledge of what is already reflected in current prices, and how other investors will react to new developments.

- Are any of these potential market impacts likely to be material over my investment horizon?

Many events that seem consequential in the near-term are immaterial to long-term investment returns. Long-term equity market returns are high despite frequent bouts of geopolitical uncertainty.

- Have my investment objectives changed in any way?

The temptation to change your approach during times of stress can be strong, but it is critical to ask whether there has been any change to your long-run goals. If not, you may just be reacting to short-term market anxiety.

- Is my portfolio appropriately diversified for a range of possible outcomes?

The purpose of diversifying a portfolio is to ensure it is resilient to a range of future outcomes. Prudent diversification means that you do not need to worry about making unreliable market predictions.

Assuming an investor’s portfolio has been carefully constructed, then the answer to the first four questions will be “no” and to the final one a resounding “yes”. This is not to say these types of events shouldn’t be factored into portfolios. As Robin Ellis, SJP’s Director of Portfolio Management commented, this week’s events are a reminder of the importance of diversification, discipline and a long-term mindset. Robin highlighted that it’s more often the preparation, ensuing portfolios are diversified before bouts of market volatility that are more important than reactive moves taken during a crisis.

Market events like this are highly uncertain, evolve quickly and cause significant market fluctuations. While tempting, trying to predict how these will unfold can destroy value over the long term. Looking through the noise, remaining invested and allowing returns to compound over the long term is usually the best strategy in building long-term wealth.

The value of an investment with St. James's Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested. Past performance is not indicative of future performance.

BLOOMBERG®” and the Bloomberg indices listed herein (the “Indices”) are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Indices (collectively, “Bloomberg”) and have been licensed for use for certain purposes by the distributor hereof (the “Licensee”). Bloomberg is not affiliated with Licensee, and Bloomberg does not approve, endorse, review, or recommend the financial products named herein (the “Products”). Bloomberg does not guarantee the timeliness, accuracy, or completeness of any data or information relating to the Products.

Certain information contained herein, including without limitation text, data, graphs, charts (collectively, the “Information”) is the copyrighted, trade secret, trademarked and/or proprietary property of MSCI Inc. or its subsidiaries (collectively, “MSCI”), or MSCI’s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”), is provided for informational purposes only, and may not be modified, reverse-engineered, reproduced, resold or redisseminated in whole or in part, without prior written consent.

Most popular articles

Most recent articles