- Retirement

- Investing

In an increasingly volatile world, what do market ups and downs mean for those investing for their retirement?

On the surface, investing for retirement may seem straightforward – the younger you are, the more risk you might be prepared to take with your investment portfolio. For those approaching retirement, derisking their portfolio is likely to be a preferred approach.

Market swings and volatility may be perceived as having a negative effect for many people at different stages of retirement planning. People worry about being able to ‘time the market’. But what really is market volatility and how can you use it to your advantage in your retirement portfolio?

At a glance

- You can help manage the volatility risk of your retirement portfolio by choosing the level of risk you are willing to take across your ISA, pension and other investment products. Diversification also helps to manage volatility risk.

- Even though volatility can be nerve-racking for investors, history suggests it is important to remain invested in tough times to benefit from the long-term gains of investing.

- Market volatility could potentially help those who make regular contributions to their investments accelerate portfolio growth.

Market volatility is a measure of how much the price of an asset fluctuates over time. Periods of high volatility are defined by unpredictable, abrupt price swings, whereas low volatility means more stable asset price movements.

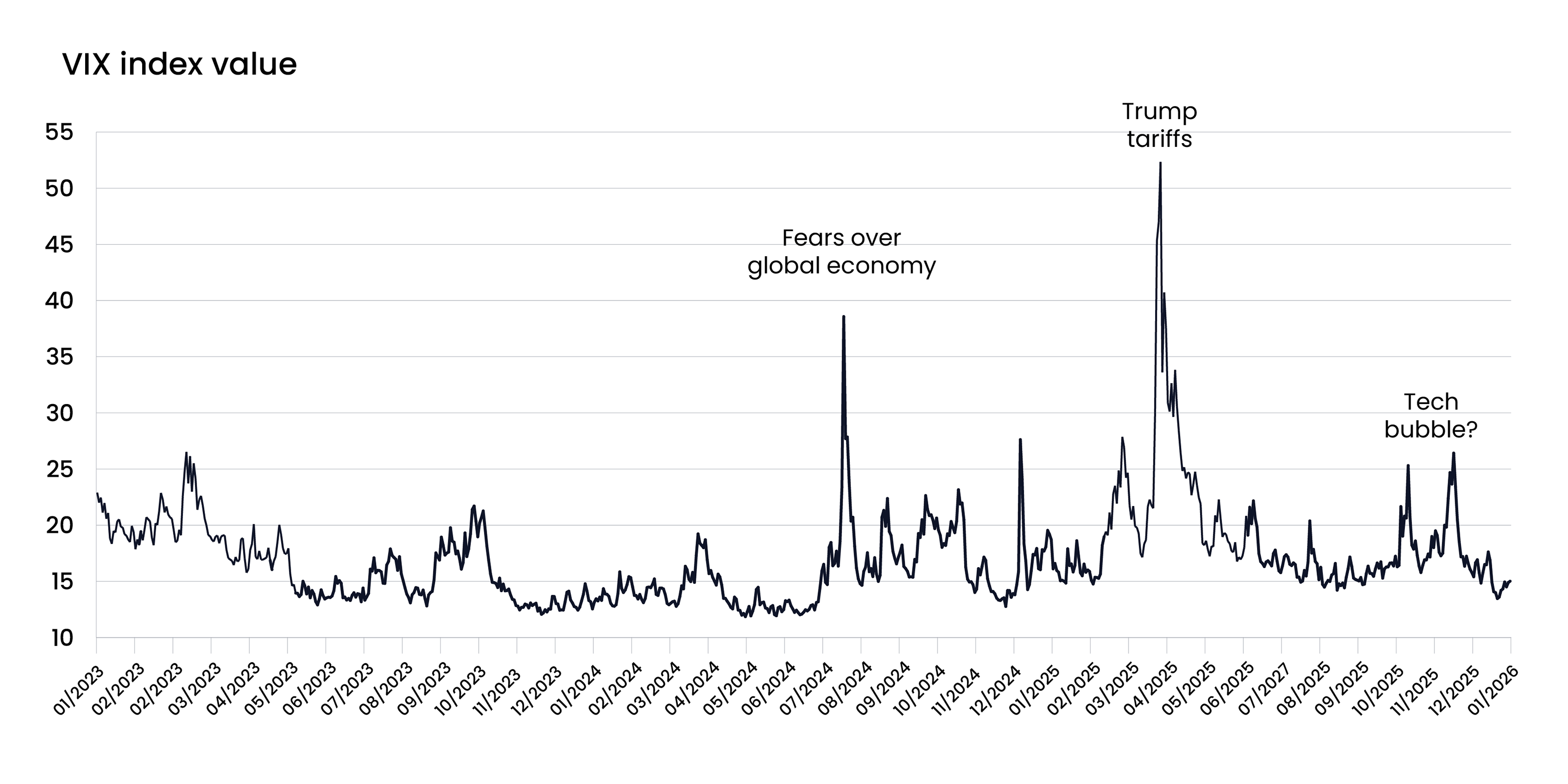

The financial markets experienced periods of high volatility back in April 2025, when US President Donald Trump announced tariffs on imports from many countries. Later in November, the S&P 500 experienced a fall when investors became anxious over fears of overvalued technology stocks. The index later stabilised when the market reacted positively after the Federal Reserve said it would cut interest rates further, boosting investor optimism.

Many financial markets experts look to the VIX index to understand sentiment across the equity market. The VIX provides a measure of volativity and the expectation of future price changes in the S&P 500.

Source: Bloomberg. Data as of 6 January 2026.

But how is this volatility relevant to your investments, and how can it affect them?

Time is of the essence

Volatility is typically caused by uncertainty from economic, political or company-specific factors. When professional financial planners are making assessments on the level of volatility in their clients’ portfolios, they pay particular attention to their investing timeframe. For instance, if you are close to retirement, your portfolio might have less time to recover from any potential losses and therefore it makes sense to protect it from high volatility. Conversely, if retirement is a long way away, your portfolio has more time to potentially recover from higher volatility periods and outgrow any losses.

This means keeping your portfolio invested for as long as possible makes it more likely these short-term market shocks will be smoothed out.

In any case, high volatility can be unsettling; after all, the money you are investing is at risk. It may be tempting to sell shares in the belief that this will protect you against further losses.

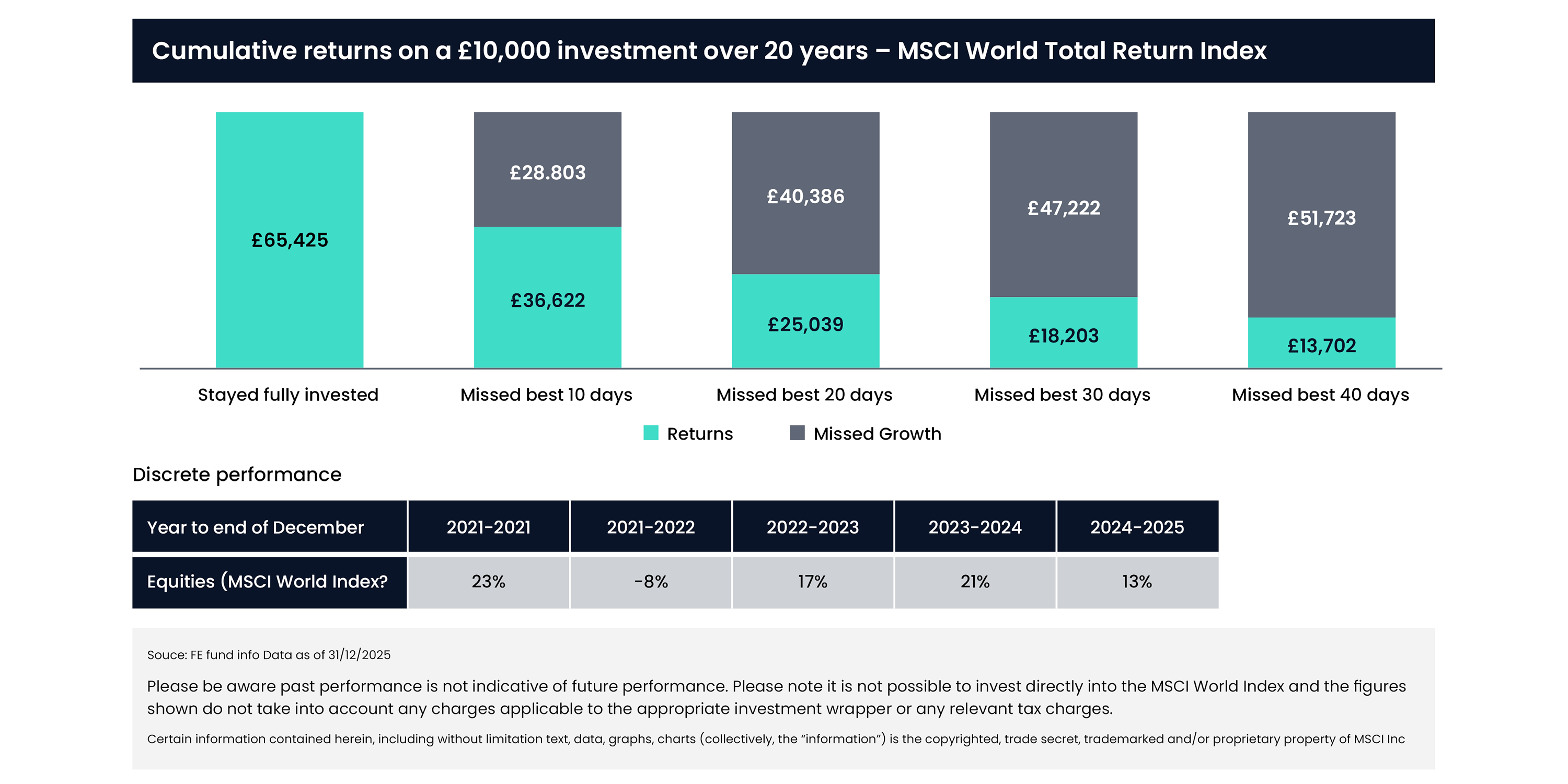

But history suggests that when the temptation to sell out feels strongest is in fact the point when it is most important to stay invested, as the chart below illustrates.

Cumulative returns on a £10,000 investment over 20 years - MSCI World Total Return Index.

If you had invested £10,000 in the MSCI World Total Return Index 20 years ago and kept it untouched, your pot would have grown to £65,425. But if you instead chose to sell off and missed the 10 best-performing days, your pot would have grown to £36,622, resulting in a £28,803 difference.

Making the most of ups and downs

It is no secret that volatility has a negative reputation, but its advantages are less well known and leveraged.

If you regularly put money into a pension or make other regular contributions across your investments, you are increasing your chances of benefiting from one of the effects of volatility. When volatility is high, investors tend to sell their assets, making prices go down. Conversely, in a low-volatility environment asset prices tend to go up.

If you invest regularly, you are buying more of an asset when prices are lower and less of that asset when prices are higher. Buying cheaper assets during a downturn could result in quicker growth when markets begin moving upwards.

This strategy of investing a fixed amount at regular intervals is called pound-cost averaging. It has the potential to deliver growth as it reduces the risk of trying to time the market.

Claire Trott, Head of Advice at St. James’s Place, says: “For most of us, we receive a regular income so paying each month into our pension rather than waiting until the end of the year makes sense in many ways. Firstly, some of your funds will be invested for longer, and secondly, you can benefit from pound-cost averaging rather than taking the risk that at the end of the year will be the right time to invest.”

Many eggs, many baskets

There are ways for investors to reduce exposure to volatility, one of which is through portfolio diversification.

Diversification can be achieved in different ways. For instance, in an equities portfolio, diversification could happen through a combination of different sectors, industries or geographies.

But looking more broadly at what makes up a portfolio, diversification could mean a blend of different asset classes.

Concentration in a portfolio works as long as its assets are growing; but if these assets take a hit, there are no other parts of your portfolio to potentially offset these losses.

Diversification plays a part in managing the volatility of a portfolio by offsetting losses in one part with gains in other parts. For instance, a portfolio with investments exposed to different asset classes, such as equities and bonds, should have less exposure to volatility when it happens across specific parts of the market.

Many asset managers, including St. James’s Place, place diversification at the core of their investment principles aiming to improve investment outcomes. A financial adviser should be best placed to guide you through the best way to choose the right portfolio based on your appetite for risk.

The value of an investment with St. James's Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested. Past performance is not indicative of future performance.

The favourable tax treatment of ISAs may not be maintained in the future and is subject to changes in legislation.

The information does not constitute advice and should not be relied on as such. It does not constitute a recommendation or an offer or solicitation. No responsibility can be accepted for any loss arising from action taken or refrained from based on this publication.

Certain information contained herein, including without limitation text, data, graphs, charts (collectively, the “Information”) is the copyrighted, trade secret, trademarked and/or proprietary property of MSCI Inc. or its subsidiaries (collectively, “MSCI”), or MSCI's licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”), is provided for informational purposes only, and may not be modified, reverse-engineered, reproduced, resold or redisseminated in whole or in part, without prior written consent.

BLOOMBERG®” and the Bloomberg indices listed herein (the “Indices”) are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Indices (collectively, “Bloomberg”) and have been licensed for use for certain purposes by the distributor hereof (the “Licensee”). Bloomberg is not affiliated with Licensee, and Bloomberg does not approve, endorse, review, or recommend the financial products named herein (the “Products”). Bloomberg does not guarantee the timeliness, accuracy, or completeness of any data or information relating to the Products.

© S&P Dow Jones Indices LLC 2026 .

Most popular articles

Most recent articles