- Investing

- News

With US mega caps hogging headlines, are investors ignoring the potential in the East?

At a glance

- Chinese equities have underperformed Western peers since Covid

- Despite recovering in 2025, does the Chinese market remain relatively undervalued?

- With its own strengths and weaknesses, the Chinese market could act as a diversifier to Western equities.

Who do you think the global leaders in robotics are? A quick look online might bring up familiar US brands. Potentially Tesla robotaxis. Or Amazon, with its warehouse robots.

While these household names are undoubtedly making great strides, the reality is that the scale of robotics in the US, and in fact the entire West, pales in comparison to China.

According to the International Federation of Robotics, China accounted for 54% of all industrial robot installations in 20241. And that percentage is expected to grow in coming years.

There are similar stats in other areas. Backed by the country’s near-monopoly on rare earth metals, Chinese companies produce over 80% of global solar panels2.

Even in areas long the preserve of Western dominance, China is fast catching up. Chinese car brand BYD saw sales in the UK grow 880% between September 2024 and 2025. Its 11,271 registrations put it ahead of household names like Citroën, Honda and Renault. It also leapfrogged EV rival Tesla, by sales over this period3.

China is a global manufacturing powerhouse, and increasingly a hub for high-tech developments. According to Martin W. Hennecke, Head of Asia & Middle East

Investment Advisory at SJP: “Technology-wise, China is stunning. They used to have a reputation for being good at copying developments elsewhere. Now, China is the world’s largest R&D spender, leading in many fields beyond the well-known areas from deep-sea drilling to high-speed rail and nuclear energy, whilst catching up rapidly in others having leapfrogged the EU in novel drugs, nearly catching up to the US’s count.”

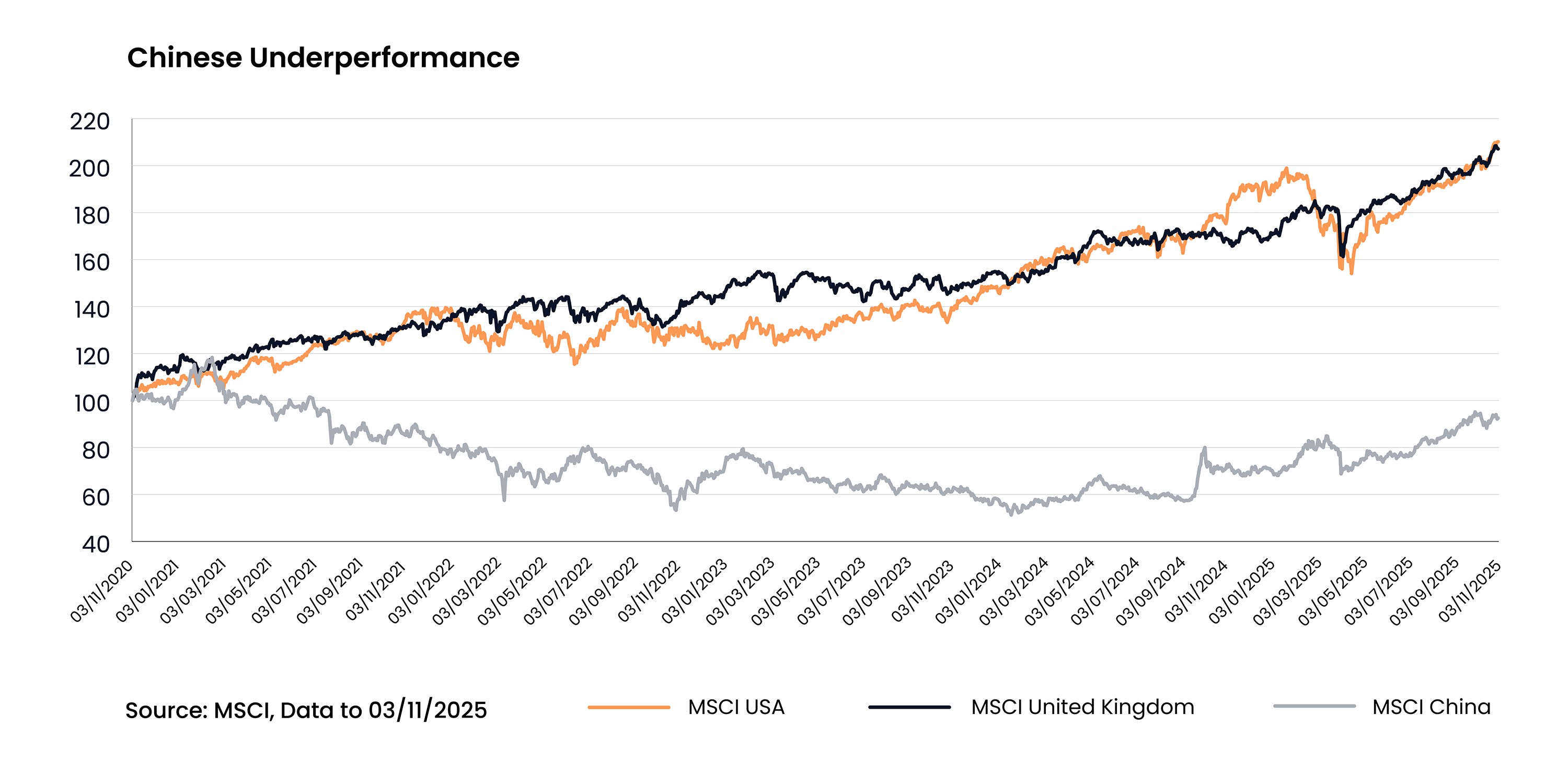

However, the rise of Chinese technology has not been equally matched by its stock market over recent years. In fact, despite strong performance over 2025, Chinese equities are below where they were five years ago. In comparison, both the MSCI US and MSCI UK have more than doubled in that time.

| 03/11/2025 - 03/11/2025 |

03/11/2023 - 03/11/2024 |

03/11/2022 - 03/11/2025 |

03/11/2021 - 03/11/2022 |

03/11/202 - 03/11/2021 |

|

| MSCI United Kingdom | 22.66% | 14.33% | 6.91% | 5.53% | 30.91% |

| MSCI USA | 19.38% | 27.04% | 7.20% | -3.59% | 34.09% |

| MSCI China | 31.04% | 14.51% | 6.27% | -31.92% | -14.78% |

Past performance is not indicative of future performance. Please note it is not possible to invest directly into an Index

Politics and property

Much of this underperformance can be attributed to a property bubble bursting, as well as political decisions taken by the government.

The phenomenon of ‘ghost cities’ across the country symbolised an overheating property market in the 2010s. The poster child for the bubble was Evergrande. The company was worth over $50 billion at its peak in 2017 and was responsible for hundreds of projects – largely financed by debt. By 2024, proceedings to wind the company up were issued, and it was finally delisted this year.

While the property bubble was bursting, the government also moved to reduce the power of large tech companies. Jack Ma, co-founder of Alibaba, temporarily disappeared from public view shortly after appearing to criticise the Chinese regulator, while his fintech Ant Group’s $37 billion IPO was suddenly stopped.

To cap it all off, Chinese and US trade frictions became increasingly pronounced. This meant increasing tariffs, higher costs, and limited access to technology like semiconductors. All of which has stunted Chinese valuations.

A potential turnaround?

Nothing lasts forever, however, and 2025 saw the beginning of a turnaround. The Chinese government, noting the poor stock performance of many of its companies, became more business friendly.

According to Martin: “The Chinese Government seemed to say ‘enough is enough. We like private enterprise; we like home-grown tech and want to support it’.

You can see that in how they started rolling out support measures for the real estate sector. They also added liquidity to support growth companies, partly prompted by US tech sanctions.”

Outside of domestic politics, some of the combative trade talks of 2025 have helped shine a light on the innate strength of the Chinese economy. For example, despite wide awareness of China’s monopoly on rare earth minerals, others have struggled to build capacity of their own at the scale required.

All this has allowed Chinese companies to stage something of a recovery of late. Between the start of the year and the start of November, the MSCI China Index grew 30%. Even after this growth, there remain numerous companies with attractive valuations.

Challenges remain

With a fast-developing base and relatively low valuations, China can offer investors an opportunity. But challenges remain.

Much ink has been spilled commenting on Chinese demographic challenges, while trade relations between China and the US remain uncertain.

On top of this, there are differences between the Chinese and US market to be aware of.

In the US, there are many industries with dominant established players relatively secure in their position. The Magnificent 7 are the biggest examples, but even outside of technology, there are lots of companies who would be hard to challenge in the short term. Think about the brand power of Coca Cola or McDonalds, or the logistical hurdles required to compete with Walmart, for example.

In contrast, the Chinese industry is younger, with more challengers, and the big players are less able to rely on inertia to carry them forward. Although

BYD is over 20 years old, most of its explosive growth has occurred in the past five or so years. Temu is a recent household name, challenging established players such as Alibaba and Shein in a way few Western companies could challenge Amazon.

Potential diversifier

Looking longer-term, Chinese markets may occupy an interesting place as a diversifier within portfolios.

Martin concludes: “We’ve had five years of US markets rising sharply while Chinese equities dropped. But markets can shift, and money has to go somewhere. China hasn’t been very correlated to the US in recent years, so even if US markets should see a drawdown, it is possible that China could rise at the same time.”

The value of an investment with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

Past performance is not indicative of future performance.

Certain information contained herein, including without limitation text, data, graphs, charts (collectively, the “Information”) is the copyrighted, trade secret, trademarked and/or proprietary property of MSCI Inc. or its subsidiaries (collectively, “MSCI”), or MSCI’s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”), is provided for informational purposes only, and may not be modified, reverse-engineered, reproduced, resold or redisseminated in whole or in part, without prior written consent.

This information does not constitute advice and should not be relied on as such. It does not constitute a recommendation or an offer or solicitation. No responsibility can be accepted for any loss arising from action taken or refrained from based on this article. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted.

Sources

1International Federation of Robotics - September 2025

2StatRanker - May 2025

3The Society of Motor Manufacturers and Traders - accessed 4 October 2025

Most popular articles

Most recent articles