- Investing

- News

The American dream is beginning to look more tarnished. The US-Iran war, combined with volatile and unpredictable behaviour by the US president and his administration, have taken the shine off. Meanwhile the divide between the ‘haves’ and the ‘have nots’ is growing ever larger. We look at what this might mean for investments in the region.

At a glance

- In recent years, the gap between rich and poor has been growing in the US.

- With consumer spending an important part of the US economy, this gap is a potential vulnerability.

- Since 2024, poorer households have been harder hit by inflation and a slowdown in wage growth.

In 18th Century France, when told peasants couldn’t afford bread, Queen Marie-Antoinette supposedly said, ‘let them eat cake.’ This oft-repeated tale never actually happened, but its popularity highlights the wealth disparity the country faced in the lead up to the revolution.

Fast forward over 200 years, and the US has supplanted France as the world’s greatest power. Thankfully, centuries of progress mean the levels of deprivation found back then are no longer so widespread in the world’s leading economies.

However, the wealth disparity between the haves and have nots has been growing in recent years. Currently, the bottom 50% of the population hold just 2.5% of the total US net worth.

Since Covid, the US economy has been one of the highlights of the global economy. It has managed impressive growth, undaunted by a growing national debt pile and international pressures.

The question is, could this inequality become a threat to the longer-term growth story?

The virtuous ‘have’ cycle

One of the defining trends of the post-pandemic period has been the performance of equity markets. Following a drop at the start of the pandemic, equities recovered relatively quickly and then seemed to go from strength to strength (although the Iran conflict has somewhat muddied the picture since it began).

Until relatively recently, US equities were among the best performing markets.

This has been partly driven by a consumer base that left the pandemic with greater savings than they went into it with. Wealthier families built up notably larger savings buffers, allowing them to continue spending even when times get tough. This keeps the US economy growing and equities rising.

Those same household groups are also likely to hold investments. As they spent, equity prices went up, meaning the wealth of the better-off households grew as a whole.

In other words, spending by wealthy households helped push up prices. These same households then benefit from the equity performance their spending is helping generate, further boosting their wealth. In recent years, this has formed a virtuous circle for better-off households.

In comparison, those in lower income brackets may still be spending, but they lack the savings buffer and are less likely to hold substantial investments. Consequently, they benefit less, proportionally, from a strong stock market.

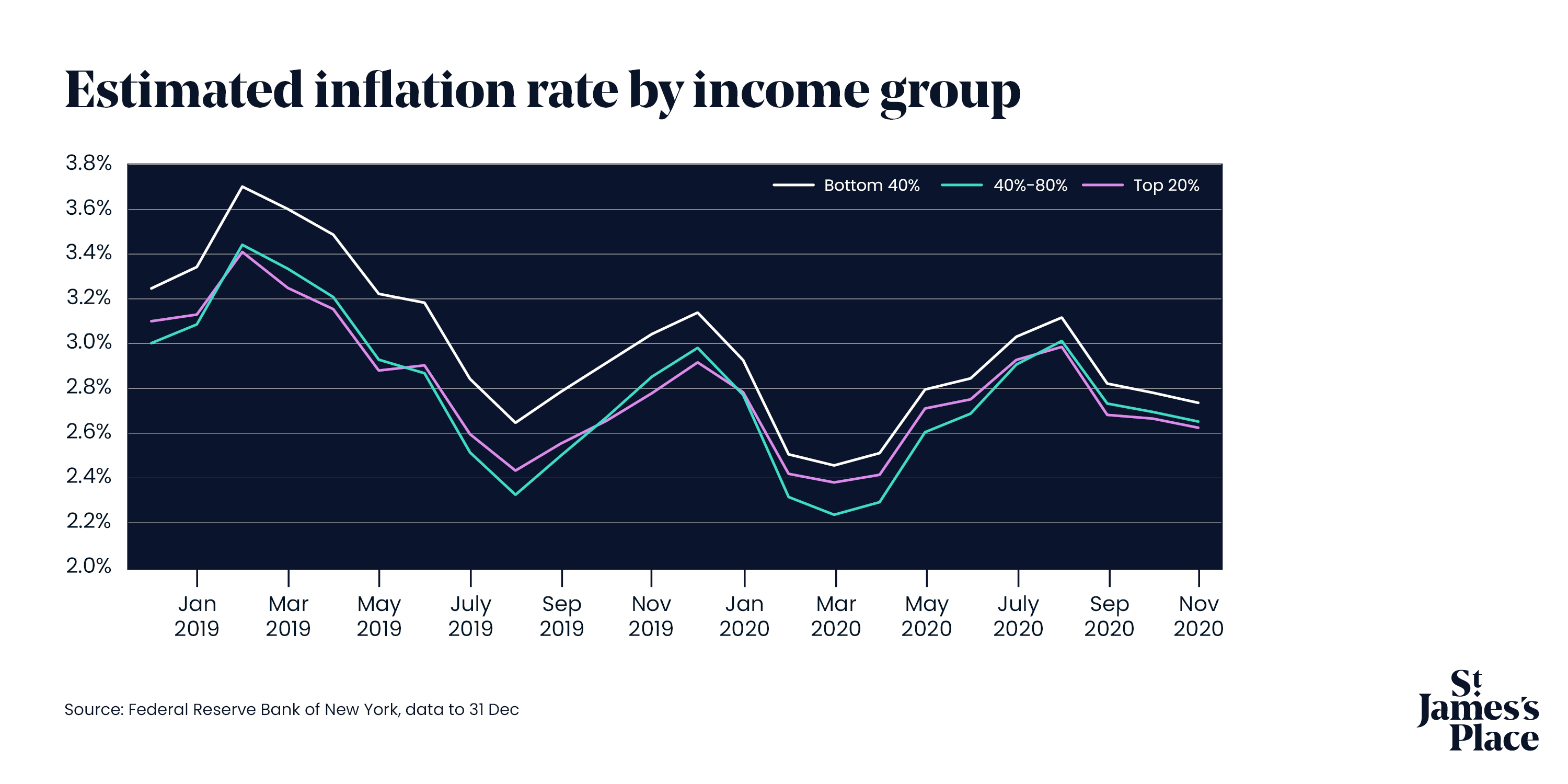

The wage and inflation gaps

The ongoing battle with inflation has also helped widen the gap between different income groups.

On a fundamental level, lower-income groups were more affected by the inflation levels that followed Covid. Those earning less are required to spend a higher proportion of their income on day-to-day utilities, energy and food. These areas have seen price volatility, meaning lower-income households have been more affected.

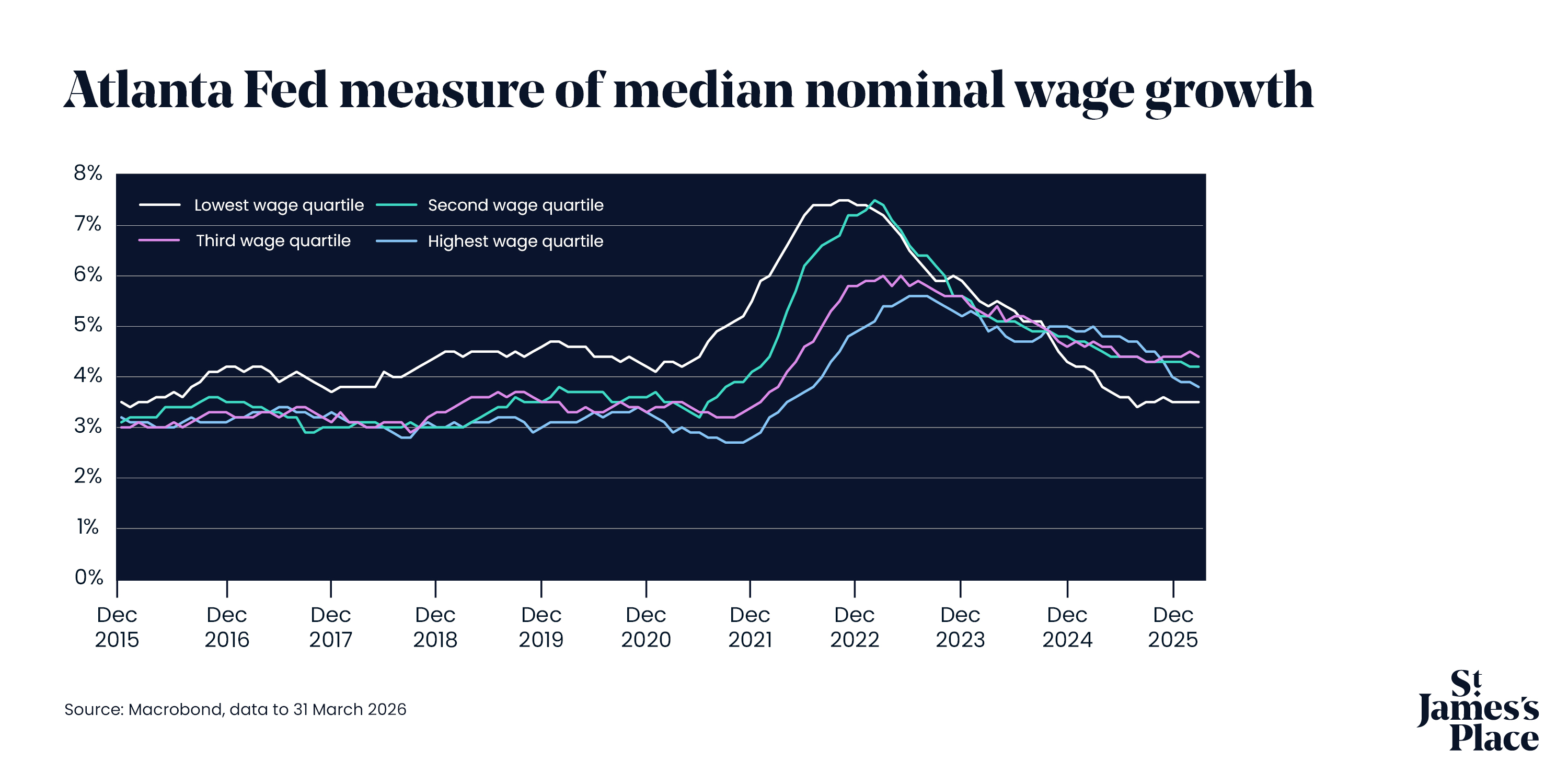

This has been made worse by a disparity in wage growth. Over the last year and a half, low-income wage growth has been notably lower than for those in higher income brackets.

As Hetal Mehta, chief economist at SJP says: “If you’re in the lower income brackets, not only do you have less in absolute terms, but it's also growing at a much slower pace than it is for other income cohorts.”

Turning a virtuous cycle into a vicious one

The reality is that the US has had a large wealth disparity for years. Although the gap is currently widening, there was a greater disparity in the aftermath of the global financial crisis than there is today. Yet the US economy has continued to grow.

As such, it is reasonable to question if an increasingly K-shaped economy is relevant for investors.

Hetal notes: “The fragility is around where we think a correction is possible or likely.”

Household savings have been key to powering much of the post-Covid economy, allowing consumers to keep spending even in tough times. Now, those savings are largely reduced – meaning a prior buffer no longer exists.

On top of this, the labour market has been cooling. Job and wage growth have both been on a notable downward trend since 2023.

At Hetal points out: “Consumer spending was supporting and supported by buoyant markets, effectively. There was the virtuous circularity.

“Now you've got employment and nominal wage growth both slowing down. You don't have strong labour incomes and you also no longer have that savings buffer. In other words, if there is another shock or wider slowdown, that virtuous cycle could start to turn vicious.”

How important is it?

As mentioned, the K-shaped economy is one of a number of risks to consider. It doesn’t mean the US economy is destined to fail, or that equities will necessarily fall. The US remains the world's biggest economy and is home to thousands of companies, including some of the biggest and most innovative ones.

But it does add a layer of fragility to the country. With the Iran conflict playing havoc with the global economy, this may be something that becomes increasingly relevant in the future. Especially as much of the savings buffer that protected many US households post-Covid has now been used up.

In this way, the K-shaped economy remains an important part of SJP’s asset allocation discussion. Whatever happens in Iran, the health of the general US consumer base will play an important part in how the world moves on – whatever comes next.

Past performance is not a reliable indicator of future performance.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

Source

1Board of Governors of the Federal Reserve System (US) via FRED – January 2026

Most popular articles

Most recent articles