SJP Achieving your pension goals

Your pension is a longer-term investment, designed to help you to build the capital that you are likely to need to live on during your retirement.

It’s likely you will need a sizable fund by the time you decide to retire, and investment growth will play an important part in achieving this. However there are also other aspects to investing in your pension that are worth being aware of that can help you to achieve your goal; these include salary sacrifice, compounding and pound cost averaging.

The value of an investment with St. James's Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

Salary sacrifice

Salary sacrifice is a term that you may come across when it comes to contributing to your workplace pension. This is where you can give up, or ‘sacrifice’ part of your salary, and possibly some of your bonus, which your employer then pays as a contribution into your pension.

What this means is that you elect to reduce your salary, and the equivalent amount is then shown as a pension contribution, paid by your employer, in the gross section of your payslip.

This can have several advantages, the main one being a reduction in national insurance (NI), for you and the employer. The difference in NI savings may possibly be added to your pension contribution by your employer as well.

A word of caution though – there are a few different methods of salary sacrifice, and reducing your salary could affect other areas of your finances or benefits, so take financial advice to make sure it is right for you.

The levels and bases of taxation and reliefs from taxation can change at any time. The value of any tax relief depends on individual circumstances.

Diverse approach to investing

Having a diverse approach to investing for your retirement is important, not only to manage your investment risk, but to give you a spread of underlying assets to better cope with changes in economic conditions.

At St. James’s Place, we adopted an approach to investment management that offers clients access to fund managers across the globe that we carefully select and contract with.

To find out more about how we work, view our Investment Management Approach.

Investment Management Approach

The value of an investment with St. James's Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

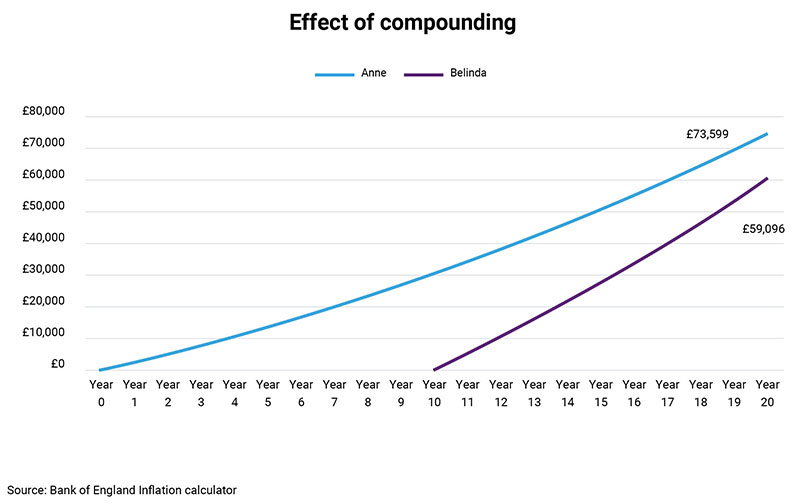

Compounding

Compounding is the growth on top of growth. You can achieve this through the interest added to savings for example, or investments where returns or dividends are reinvested.

When interest is added to your cash savings total, future interest is earned on that higher amount. It’s similar with investments. Equities (such as those found in pension investment funds) often have dividend payments, which if reinvested and added to the original capital, means your investments are growing that bit more.

Over a longer period of time, this can prove a powerful way to grow your savings and investments. This is why it’s important to start saving for retirement as soon as you can. Even if you start small, it all adds up.

These figures are only examples and are not guaranteed - they are not minimum or maximum amounts. What you will get back depends on how your investment grows and on the tax treatment of the investment. You could get back more or less than this.

However, as Anne has had the benefit of compounding for longer, her savings have grown by an extra £14,503 compared to Belinda.

Talk to your St. James’s Place Partner about how compounding can work for you.

Pound cost averaging

Getting the timing right to make lump sum investments can be difficult, especially if markets are experiencing some volatility. However, investing into a pension on a regular basis means short term volatility can beneficial over the longer term. It’s called ‘pound cost averaging’. Investing on a regular basis, you will buy more units of a fund when equity prices fall. This works to your advantage when markets rise again.

These figures are only examples and are not guaranteed - they are not minimum or maximum amounts. What you will get back depends on how your investment grows and on the tax treatment of the investment. You could get back more or less than this.

As the graph shows, over the course of 12 months, 'Investment A' experienced a rising market. This means fewer units were bought each month as the unit price went up, resulting in 8,380 units after 12 months.

'Investment B' experienced a falling market that then recovered back to the starting level. This fund is worth more after 12 months because more units were bought (19,792) in total.

To find out more, speak to your St. James’s Place Partner, or find an adviser.

Let us help you find a local adviser

Find a local adviser

Let us help you find your local financial adviser

Find your local financial adviser