SJP Risks in retirement

Most people will be aware of and recognise ‘investment risk’; the fluctuations in the value of your investments as the stock markets go up and down.

This is a fact of life, especially when you are building your retirement wealth over many years.

However, when you are ‘in retirement’ and decide to access your pension savings there are additional risks to be aware of that can have a detrimental impact if left unchecked.

Having some understanding of how these work can be useful, and to include in your regular reviews with your St. James’s Place Partner.

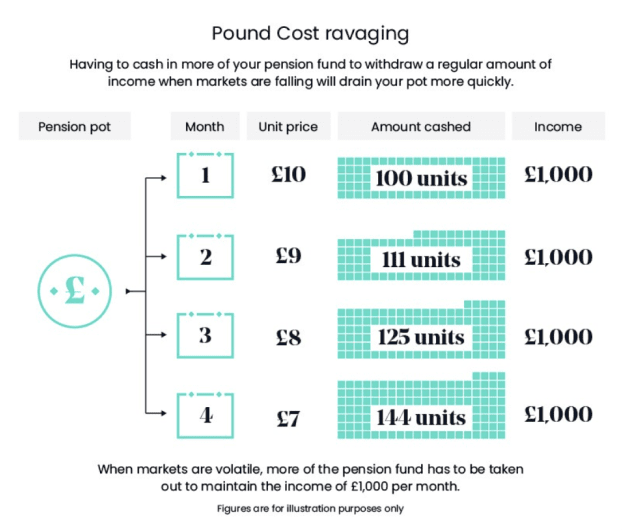

Pound cost ravaging and sequencing risk

Negative pound cost averaging, or ‘pound cost ravaging’ is the effect on your pension of having to cash in increasing amounts of your pension funds, in order to support a withdrawal of a regular monetary amount of income, when markets are falling.

This is because, when the unit price of your investments falls, more units have to be encashed in order to maintain the same amount of required income.

The diagram shows that as the unit price falls, which reflects the market falling, more of the pension fund has to be withdrawn in order to maintain the fixed income figure of £1,000 per month.

Pound cost ravaging is a component part of sequencing risk, but sequencing risk addresses the order in which you receive good or poor returns when you start drawing down an income.

Sequencing risk is crucially important; if you get off to a poor start when you begin drawing your income from your pension, such as when markets are falling and returns are negative, your investment is placed under increased pressure from outset.

The result is that your pension funds will have a harder time recovering over the longer term compared to if markets were rising at outset.

These figures are only examples and are not guaranteed - they are not minimum or maximum amounts. What you will get back depends on how your investment grows and on the tax treatment of the investment. You could get back more or less than this.

The diagram shows a comparison between having a good and poor start; both examples have an average return over 10 years of 6%, and withdraw £7,000 of income annually from an initial fund of £100,000.

However by year 10 there is a £47,653 difference in values, highlighting how poor returns in the early years when you start taking income, can have a long term detrimental effect, even if you achieved the same average returns.

There are ways in which you can mitigate sequencing and pound cost ravaging. During volatile markets, your St. James’s Place Partner will be able to help you to consider the best ways to manage your retirement income, and preserve your hard earned retirement wealth.

Inflation risk

Inflation is a risk that persists into retirement. It’s a fact of life that we can’t get away from, but it can often be overlooked.

In fact, not only can inflation eat away at the value of your income’s purchasing power, but also at your retirement investment’s capital value.

So there are a few things to think about when you are deciding to create an income from your retirement savings.

Firstly, have you built in increases to your income, at least in line with inflation each year as part of your retirement plans?

Secondly, as you get into much older age, you may notice that your tolerance for investment risk starts to decline, with a possible move towards more cautious funds. Your investment capital will still need to grow to keep pace with inflation to retain its real value.

Lastly, think about what will happen if you withdraw your tax free cash lump sum, and put it into your bank account.

The value of an investment with St. James's Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

Longevity risk

Longevity risk is at the heart of one of the most common fears for anyone thinking about retirement; running out of money.

How can you make your money last as long as you do, or have some left over to pass on to your loved ones when you die?

The problem is that none of us know how long we are going to live for. We do know however that we are all living longer on average than ever before.

Past and Projected Life Expentency - At age 65

Source: ONS, Past and projected expectations of life, 2021

The chart shows how the life expectancy for a 65 year old has changed over time, and predicted to increase in the future.

However, the risk actually comes from underestimating how long you might live for. Additionally, your life expectancy age represents the 50/50 point, and so it is crucial to also understand the chance of living beyond that to much older age.

Underestimating your life expectancy can in turn affect your views on how much income you are willing to withdraw from your retirement savings.

Your St. James’s Place Partner will be able to help you better understand your life expectancy, and how this will change over time using sophisticated cashflow modelling software at your regular review meetings. This will help you to make better informed decisions.

Let us help you find a local adviser

Find a local adviser

Let us help you find your local financial adviser

Find your local financial adviser