- News

Welcome to the latest issue of Justin Onuekwusi, our CIO, quarterly insights.

From Old Trafford to Wall Street – it sounds like an odd pairing. But on a recent trip with my family to watch Manchester United play Burnley, I was struck by some parallels between being a football fan and investing.

The atmosphere was electric but it was a rare win for the Red Devils in an otherwise disappointing start to the season. While it has been a real privilege to be a Manchester

United supporter in my lifetime, this victory was a reminder of the importance of staying loyal through tough times. And the same can be said of investing. While setbacks can test our resolve as investors, patience inevitably pays off.

In investment, staying the course through the ups and downs is often the key to long-term success.

Geopolitics is dominating the headlines

But it can be all too easy to deviate from the original plan in the current geopolitical environment.

The war in Europe continues with no sign of end. There are tensions in trade – not least between China and the US, the world’s two largest economies.

There are elections that could reshape superpower policies and change the face of the world we live in.

However, in an historic move, Israel and Hamas have this week signed the first phase of a peace deal. This opens the way for a ceasefire and has strengthened hopes for an end to the war.

As well as the wider geopolitical risks, here in the UK investors have had to deal with challenging news coverage around the state of the UK economy and the looming Autumn Budget.

But what does this all mean for our portfolios? There is often an instinct to want to react to external events by making changes to investment portfolios.

Yet, the link between politics and equity markets is quite tenuous, with valuations typically the more meaningful driver over the medium term. It is also important to recognise that making changes at the height of volatility can impact portfolios significantly.

Does a weaker dollar mean long-term decline?

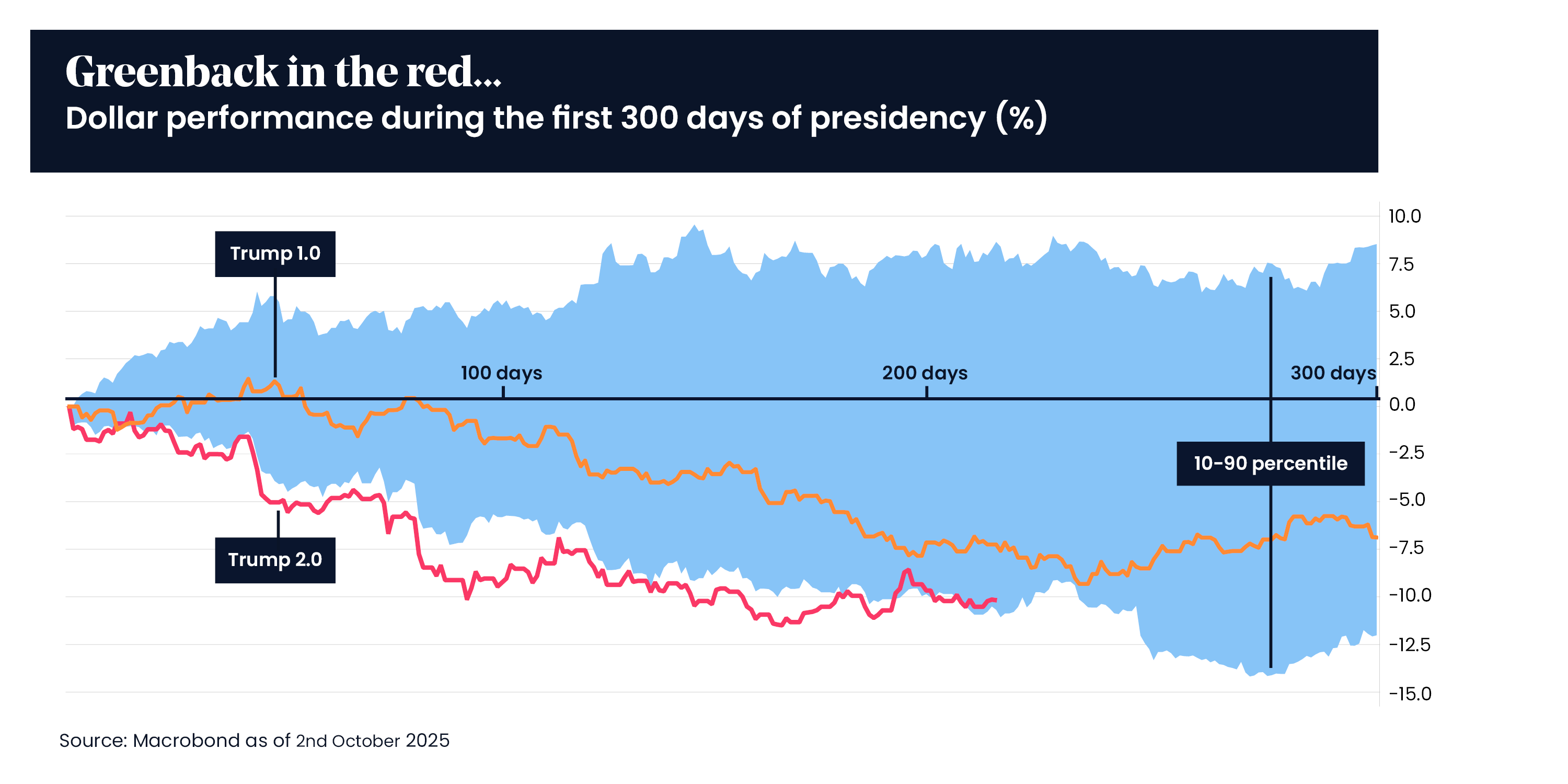

A particular theme or concern in recent months has been the US dollar, which has weakened significantly. In fact, it had its worst first half of the year in over 50 years, driven by investors selling off US assets over fears of the impact of tariffs.

Many were also fearful that the so-called ‘One Big Beautiful Bill’ would further push up US debt levels. The declining “greenback” has even led to talk that the US will lose its status as the world’s reserve currency – so-called ‘de-dollarisation’.

The chart below tracks the performance of the US dollar over the first 300 days of both Trump presidencies. The lines are showing the decline of the dollar, with both terms showing significant weakness. Notably, Trump 2.0 reflects an even

steeper drop than his first term.

It’s fair to say that US fiscal and monetary policy has been a concern. Government spending has surged and the US federal budget deficit has swelled to levels not seen in decades outside of recessionary periods.

One worry is whether political pressures could challenge central bank independence – for instance, might governments lean on central bankers to keep interest rates lower for longer to ease their debt burdens? These are the kind of “red

cap” risks (political wildcards) on the horizon that we keep on our checklist.

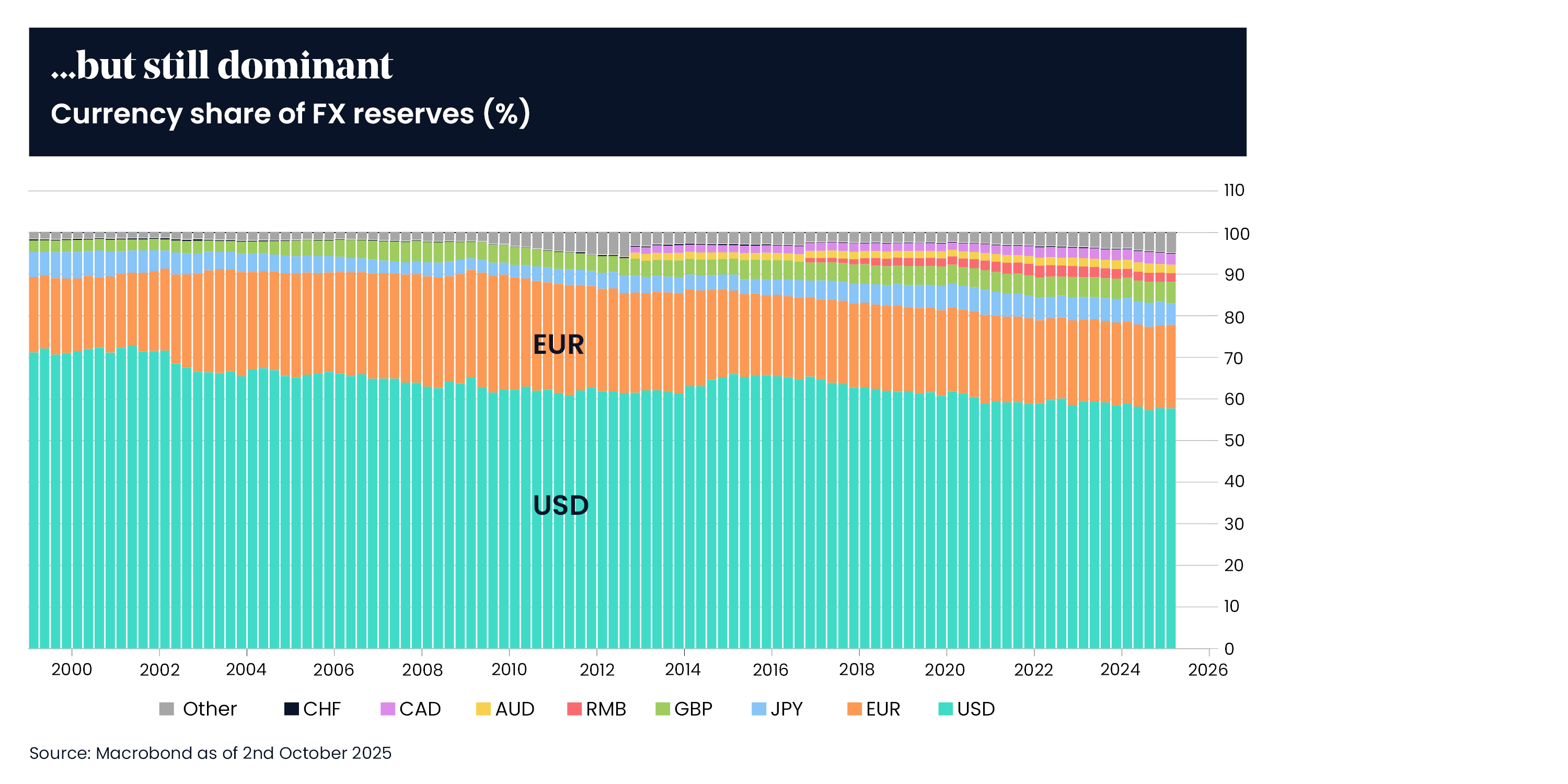

However, to paraphrase a famous quote, reports of the death of the dollar certainly appear overexaggerated. Despite recent weakness, the dollar remains the dominant global reserve currency, as the below chart shows, accounting for nearly 60% of global FX reserves. The euro trails significantly at under 20%, with other currencies such as the yen, pound and yuan comprising much smaller shares. This dominance underscores the US dollar’s structural importance in the global financial system even amid cyclical weakness or political volatility.

We continue to monitor the US dollar. However, a change of this magnitude in the global financial order would occur slowly, even over decades. The US remains our largest equity position, despite our underweight relative to market cap.

Investor discipline is key

It’s human nature to feel anxiety after setbacks and to want to do something in response. After a few bad games, football fans clamour for the manager to shake up the squad. And, after a few bad months in the market, investors often feel the urge to dramatically change course. Yet often the best action is inaction.

In an age of information overload, not reacting to the “incessant stream” of financial news and emotional triggers can feel almost impossible, as my colleague and Director of Research Joe Wiggins observes. But acting on every market dip or headline is usually counterproductive. In most aspects of life, doing less is easy – in investing it’s difficult.

Jumping in and out of the market is a bit like trying to time when Manchester United will score – you might miss the decisive moment. Once we start trading on emotion, we tend to reinforce bad habits like chasing performance (buying high) or fleeing at the bottom (selling low). It becomes a vicious cycle that hurts long-term results.

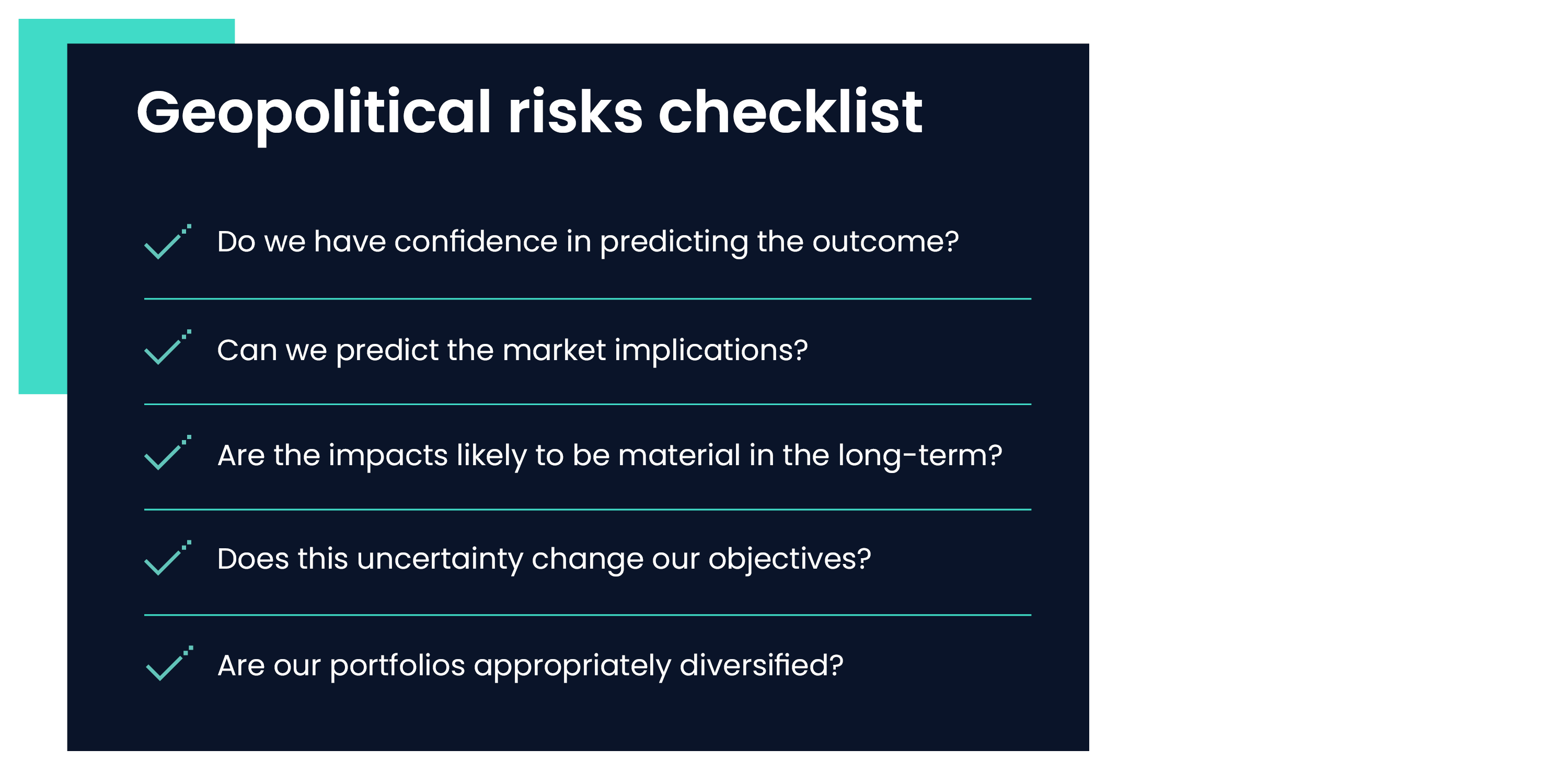

When uncertainty is high, then by definition the conviction in making any decision must be lower. Therefore, the threshold for making changes should be higher. We have created a geopolitical checklist that helps us to navigate world events in a disciplined way.

The importance of regional diversification

In the current environment, we believe diversification and resilience are key. After a long stretch where US stocks have outshone other markets, many investors have questioned the role and value of diversification.

But in my last CIO note I made the argument that US equities were riskier today than historically. This is because of the combination of extremely high US company valuations and the concentration of the US as a proportion of global equities.

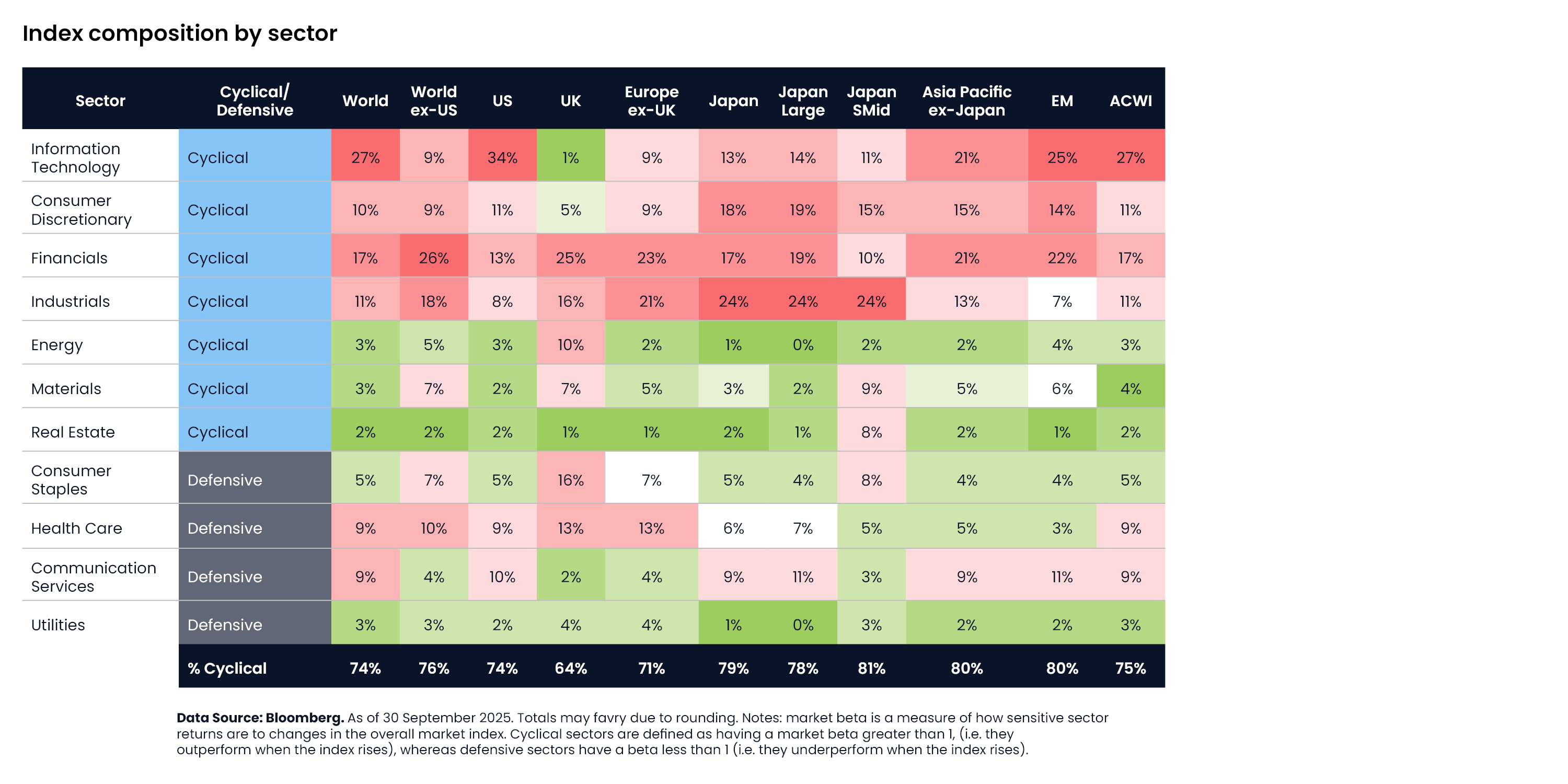

Not only is there no guarantee that the US will continue to outperform, a diversified approach is also crucial when the world is so unpredictable. The below chart shows the make-up of different equity markets across the world. It highlights how global equity markets are heavily tilted towards more cyclical sectors, with technology dominating exposures. This can make markets overly exposed to economic booms and busts. Diversification across geographies and sectors including defensives can help smooth returns, preserve capital, and reduce the risk of being overly exposed to rapid market swings.

The eclectic spread of the sectors shows the true diversity of regional equity markets to each other. To put it simply, you get different exposures when accessing different regions.

This changes over time of course. To ensure both diversification and resilience to the characteristics of different markets, we carry out thorough analysis for all our managers and the markets in which they invest.

Our position

Instead of trying to predict every political twist, we focus on making our portfolios resilient. We anchor our strategy in timeless principles, one of which is to be

disciplined.

The goal is a balance that can weather different storms. While we can’t eliminate geopolitical or macro risks, we can prepare for them through intelligent diversification and by staying the course rather than making panicked changes.

There’s a famous Warren Buffett adage that Joe highlights which captures this tension: “Wall Street makes its money on activity; you make your money on inactivity.” In other words, brokers, pundits and even fund managers profit from convincing us that constant action is required, but as investors we often profit from patience. As a loyal Manchester United supporter, I currently have little option but to remain patient.

Past performance is not indicative of future performance.

The value of an investment with St. James's Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

Most popular articles

Most recent articles