- News

Welcome to the latest issue of our CIO quarterly insights newsletter from CIO Justin Onuekwusi.

So far, 2026 has been a year of unexpected but persistent turmoil. This followed a relatively smooth end to 2025 for markets and investors. While I previously warned that investors should brace themselves for a correction - and that such corrections are also normal - few of us could have anticipated what lay ahead with the Iran conflict.

Like many, I am deeply conscious of the human impact of recent events, particularly for those with family or close connections affected by the conflicts across the world.

As Chief Investment Officer, at St. James Place it is my team’s priority to support our clients, Partners and colleagues. If recent market developments are concerning you with respect to staying on track with your financial goals, I would encourage you to speak with us or your usual contact.

Periods of uncertainty can often be catalysts for change. Right now, companies, indeed whole sectors, are adapting to shifting global trading patterns and navigating a more complex geopolitical backdrop.

The decision by the US and Israel to go to war with Iran at the end of February has seen substantial geopolitical turmoil. The conflict has spread across the wider region and for investors there is a heightened sense of uncertainty.

But what should we take from these events? Amid the noise, it is worth repeating that this situation calls for perspective rather than prediction. Reflection not reaction.

View the House and Economic views

There is no doubt global markets continue to navigate elevated uncertainty as the geopolitical situation evolves. With the Strait of Hormuz effectively blocked (at the time of writing) energy markets are at the centre of investor concern, having suffered the biggest shock seen for many years. Inflation and cost of living fears once again dominate headlines.

Through March and April (to date) prices have been driven by both news reports and statements coming from President Trump. Yet there has been less volatility than might have been expected, indicating that markets expect a short, contained shock. Too optimistic? Certainly a more sustained disruption to the world’s energy supply will have broader implications. A sustained rise in energy costs could temporarily drive up global inflation. However, while oil and energy shocks are short-term inflationary, over time demand typically adjusts and price spikes ultimately unwind.

Process and discipline

Against this backdrop, our approach remains grounded in process and discipline, rather than prediction. Prior to this event, in the last quarterly newsletter, we spoke about market declines not being unusual. We may not be able to predict what will cause these – we don’t believe anyone can do so consistently – but being prepared is key. Stressed environments increase the temptation to react or engage in speculation around inherently unpredictable events. However, this is precisely when discipline matters the most.

Why asset allocation matters – and our approach

I went to dinner with a good friend recently and I was discussing our approach for selecting the best managers across the world. These range from Kopernik, one of our active small cap managers, to State Street Investment Management, who manage our index funds in the Polaris Multi-Index funds. They asked the question, given we outsource to third-party managers, who actually owns the risk? My answer was wholeheartedly that we, the SJP investment team own the risk. We are accountable for the performance of our managers and the portfolios we have built.

Firstly, we select all of the managers you invest in utilising an extensive research process, which we believe is distinctive and differentiated from others. We have spent years hiring the most talented manager selection specialists across the UK.

Not only do we own the manager selection decisions that we make, it is also important to note that the majority of risk in any client portfolio is not driven by what managers select, but what asset class they invest in. Asset allocation is the engine of long-term returns. It’s about choosing the right mix of investments to meet client goals. So before the manager is chosen, selecting whether to invest in equities or bonds or whether to invest in the US or emerging markets is the most important decision that investors make.

The chart below shows an illustration of how much of the risk with our flagship Polaris multi-asset funds is driven by asset allocation versus manager selection:

Source: St. James’s Place, April 2026

In other words, the majority of risk comes from asset allocation and the volatility – or fluctuations – in asset classes. A minority of risk is due to manager selection.

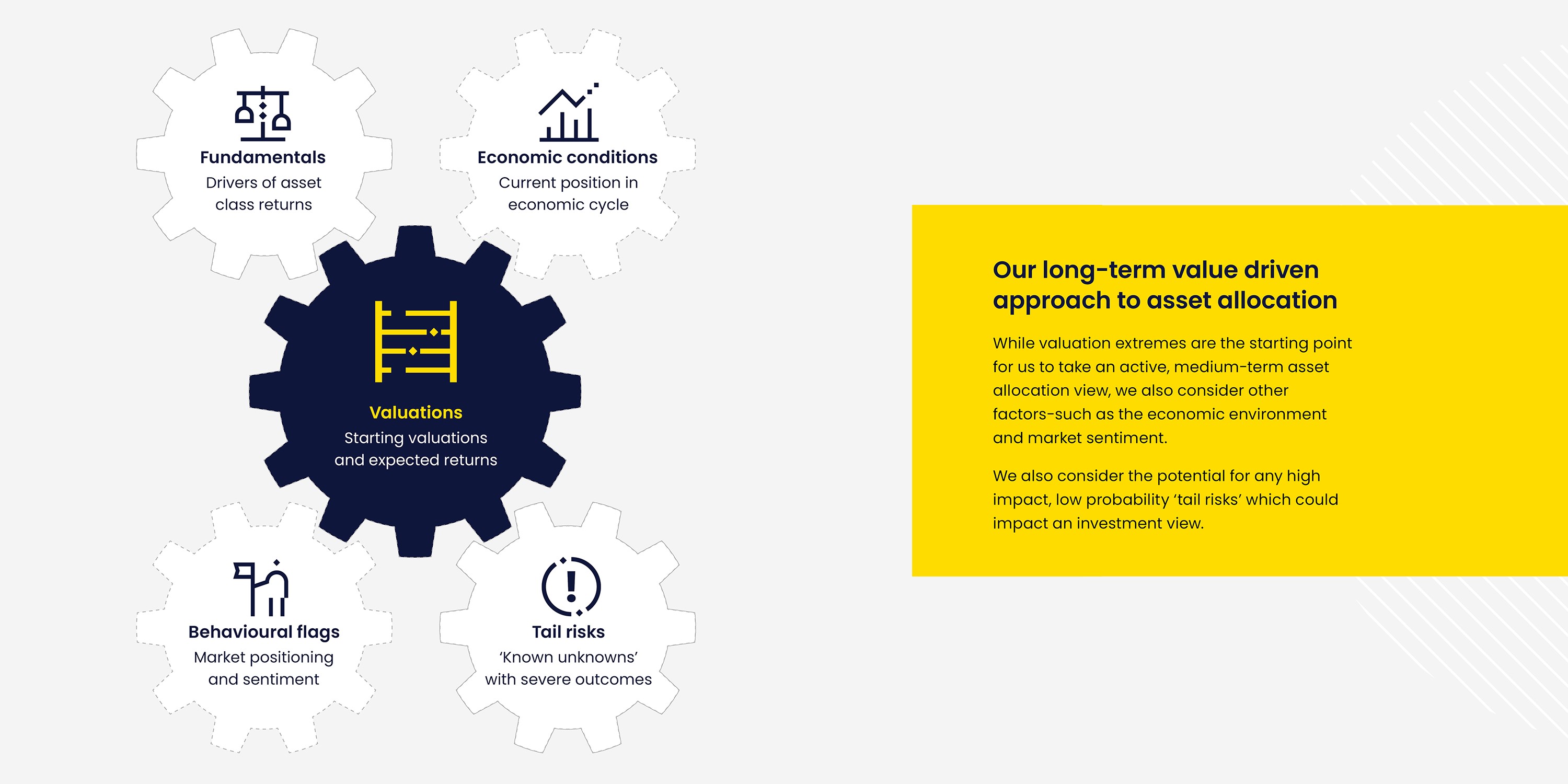

Our asset allocation process, which can be seen in our House View, begins with trying to build a diversified portfolio and focusing on valuations (i.e. whether an asset is cheap or expensive), not headlines. Research has repeatedly shown this is the biggest driver of long-term returns. The areas which are expensive tend to be vulnerable to corrections.

We look to identify where the price of assets seems out of kilter with the underlying fundamentals, whether too high or too low. We then make the decision on our allocation to that particular asset class. The chart below shows the process with the smaller cogs acting as moderators to the valuation view.

A key principle is that we avoid reacting to short-term noise and short-term tactical trading. We know markets can move quickly and sometimes for emotional reasons rather than clear fundamentals. When this happens, it can create opportunities.

Our responsibility is to make sure portfolios are positioned to withstand a range of outcomes, not to guess which path geopolitical actors will take. History shows that under stress, the likelihood of making poor, short term decisions rises sharply. Investors often mark down risky assets indiscriminately, undervaluing certain markets, and markets can shift multiple times before reaching any meaningful equilibrium. This is why discipline is essential and why staying anchored to long term objectives is far more powerful than attempting to time the market during such volatile periods.

Resilient decisions

Over the past couple of years, we have deliberately made our portfolios more robust so they can handle periods like this. That includes spreading investments more widely, adding more defensive assets such as government bonds and reducing exposure to riskier lending markets within corporate bonds. This preparation means there is less need to make hurried decisions when uncertainty is high.

We have underweighted the US market for some time. We made these decisions not because we saw the recent events coming, but rather because we look for opportunities based on valuations. To us, the concentration of the US market on the tech giants posed some risk while undervalued areas, such as the UK offered better opportunities.

That’s not to say we won’t be affected in the short-term. We are keeping a close eye on the current situation and how it may impact both the risks in our funds as well as the opportunities we see. In particular, we are watching whether higher oil and gas prices persist, whether oil producing countries such as OPEC step in, whether special energy reserves are being drawn down and how investment values settle as markets calm down. We are also reviewing our economic assumptions to reflect recent events. Is a recession more probable now? Where and what will that mean for our asset allocation positioning?

While our overall view has not changed, we are carefully assessing what the current event could mean for inflation and global growth over time.

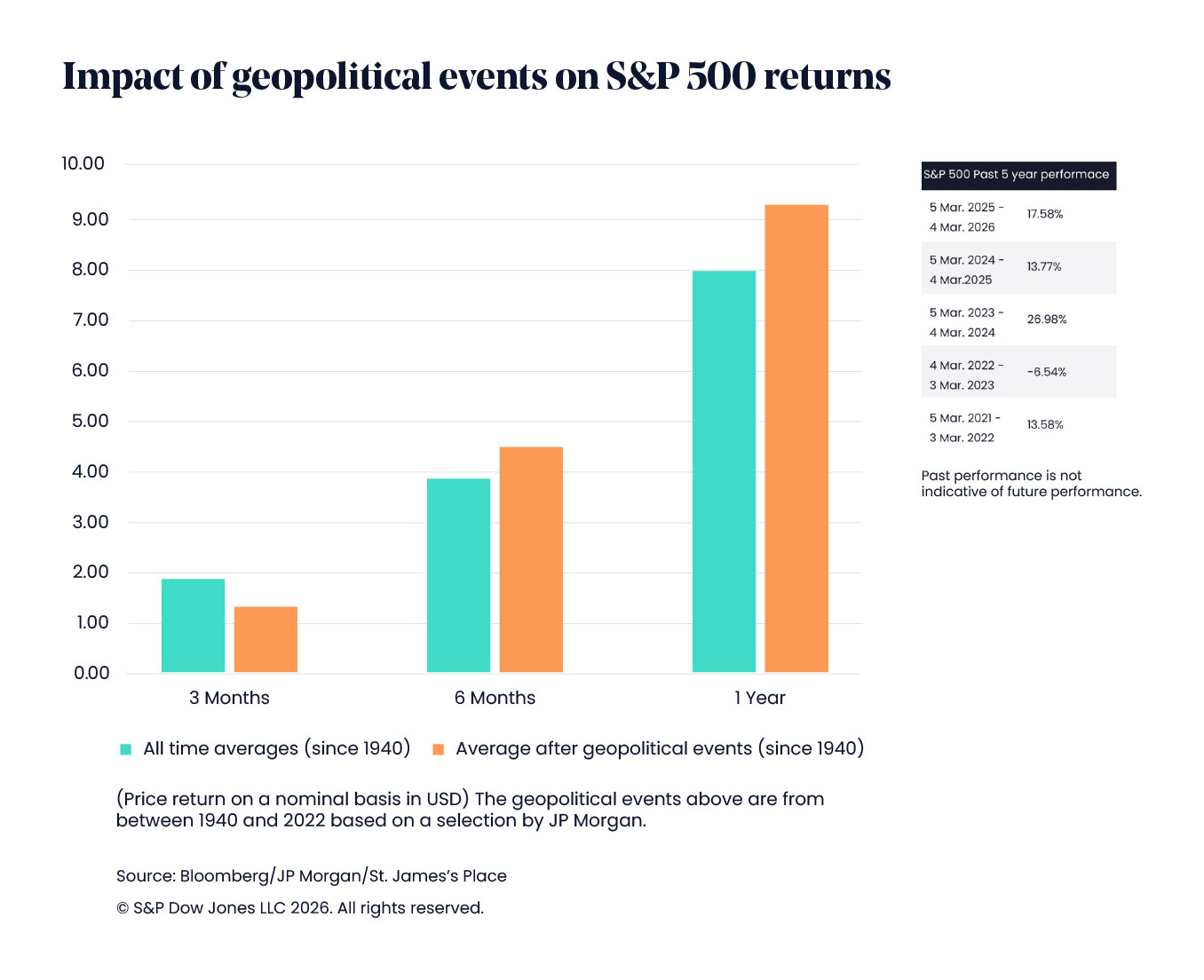

We know fear rises during complex geopolitical events. From a behavioural perspective, many investors feel a compulsion to act at times of crisis, and this may involve coming out of markets. However, as history shows us, as does the chart below, this is rarely the best decision.

Of course, there is no guarantee that markets will take this path as shown above, rather this is what has happened historically.

Inflation risks

This does not mean we are being complacent. History suggests that even when hostilities pause, second round effects can persist through energy markets and supply chains. For investors, the more durable risk is not renewed conflict itself but the inflationary consequences that can follow – particularly if higher energy, transport or insurance costs become embedded.

In this environment, inflation remains the key variable as this shapes interest rate expectations and asset valuations. This reinforces the importance of portfolio resilience, staying disciplined, diversified and focused on long term fundamentals rather than short term headlines.

Conclusion

While many news wires will point to the current geopolitical situation leading to greater uncertainty and unpredictability, we would argue that markets are always difficult to predict. Instead, when it comes to asset allocation, focusing on the long-term outcome and being disciplined with rebalancing where appropriate will ensure you continue to take the risks you intend to take, rather than those dictated by market turbulence.

For the investment team here at SJP, we fully own the risk of the portfolios we build. We took proactive action when markets were calm to build extra resilience and additional diversification. This means we are able to monitor the situation, remain disciplined and take action when necessary.

Most popular articles

Most recent articles