- News

- Investing

Post the tsunami of speculation and an unexpected and chaotic early release of the details, has Chancellor Rachel Reeves’s Autumn Budget created stability or upset? SJP’s chief economist Hetal Mehta outlines her take on what the Budget may mean for the UK economy and growth.

Raising £26 billion over the next five years through measures such as frozen personal tax thresholds, introducing national insurance on salary sacrifice contributions, as well as increased taxes on dividends, property and savings income, Chancellor Rachel Reeves has closed the “black hole” in the UK finances. Hetal Mehta, Chief Economist at SJP, says extra fiscal headroom* offers much needed flexibility to reduce policy volatility and ultimately supports economic growth.

At a glance

- Tax increases of £0.7 billion next year rising to £26 billion by 2029-2030 offset the increase in spending, which is focused on UK healthcare and defence sectors.

- The energy bill package will lower inflation in the short-term, but it doesn’t offset other effects. Overall inflation has been revised up and it most likely won’t help the Bank of England cut rates aggressively in the coming months.

- The UK productivity downgrade and resulting GDP growth downgrade in the medium term look much more realistic. Combined with the additional fiscal headroom*, there is more resilience baked into the fiscal framework.

Hetal welcomed another change regarding the Office of Budget Responsibility (OBR) assessments every six months. “The move to only one assessment a year against the fiscal rules should dampen the policy volatility and speculation.”

While the OBR downgraded medium term UK productivity, its 2025 forecast for UK growth moved up from 1% to 1.5%, commensurate with other independent forecasts.

|

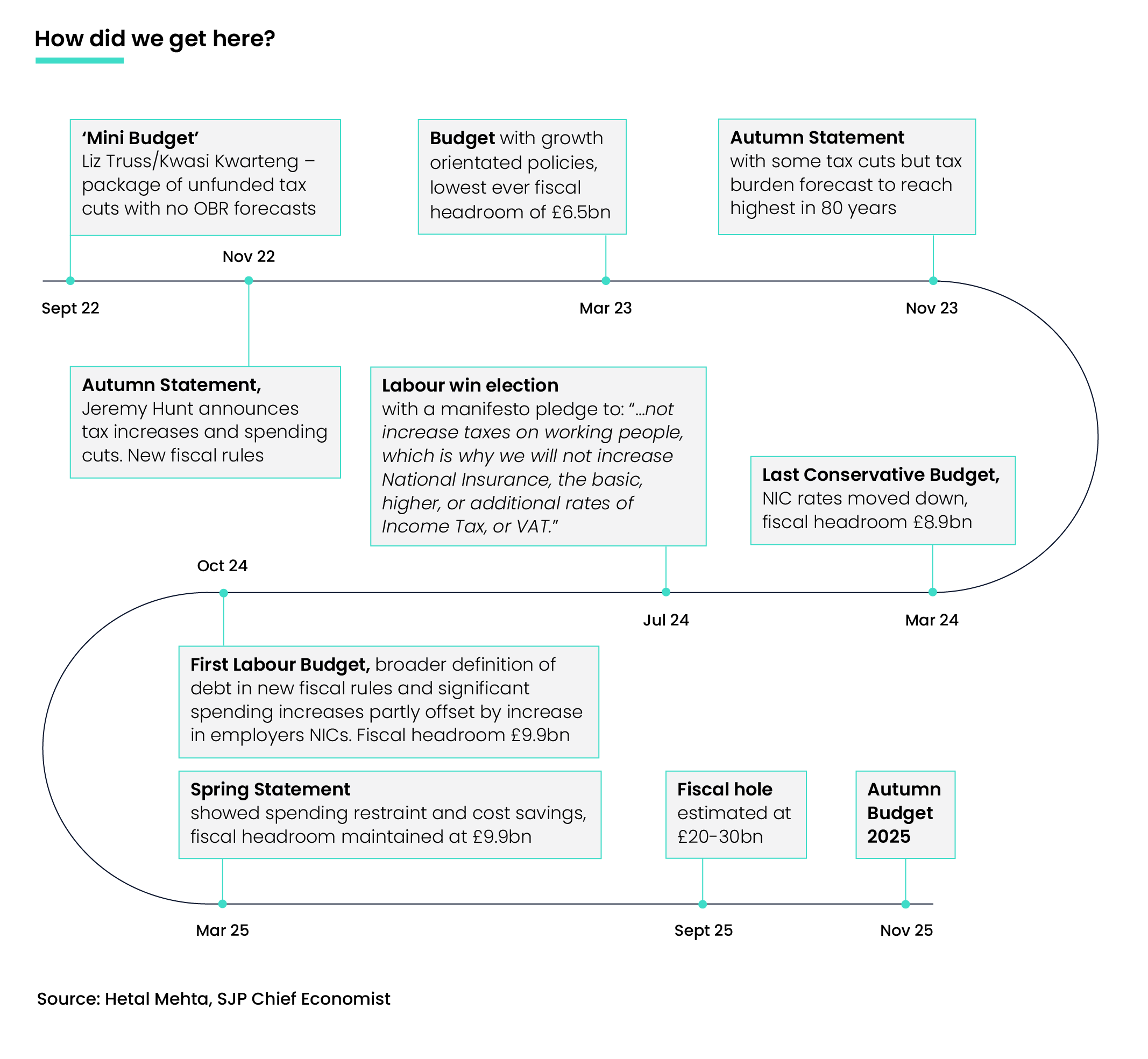

Why is the OBR so important? Considered to be a fiscal "watch dog", the Office for Budget Responsibility (OBR) provides independent analysis of the UK's finances and economic forecasts. It produces five-year forecasts on the economy twice a year - accompanying the Spring Statement and the Autumn Budget. Not only does the OBR offer an independent view of the credibility of the government's taxation and spending plans, but it can also have a big impact on market sentiment. This was particularly notable in 2022 when Liz Truss became the first prime minister since the OBR was founded in 2010 to release a Budget without the OBR doing an independent check. |

Ahead of the Budget the Chancellor faced unenviable choices says Hetal – support the economy or balance the books? Break manifesto pledges or break fiscal rules? Keep markets onside or keep voters happy? “The UK tax burden, already on track to reach around 38% - the highest on record - could climb even higher. For Reeves, there were no easy fiscal choices to make. This Budget demanded a delicate balancing act, with direct implications for households, markets, and many of our clients."

As Hetal pointed out, the economic picture heading into the Budget was mixed: GDP growth has been lacklustre, though running slightly ahead of the OBR’s expectations back in March. Inflation has remained elevated, but not as high as the Bank of England had feared, she says.

In her speech, the Chancellor says net UK debt this year will be £2.6 trillion – 86% of GDP. This means £1 in every £10 of government spending goes on debt interest.

Hetal says: “Overall, it seems the Chancellor has managed a fine balancing act. Although taxes will rise, she is also increasing spending, resulting in a very small fiscal tightening. The growth and productivity downgrades were at the upper end of expectations and now look much more realistic.”

Key announcements and forecast changes

- UK medium term productivity downgraded by 0.3 percentage points to 1% resulting in medium term GDP growth revised down from 1.8% to 1.5% (though 2025 was revised up to 1.5%)

- Overall increase in taxes by 2029/30 is £26 billion but spending will increase by £11 billion

- The fiscal headroom* has increased from £9.9 billion to £22 billion

- National Insurance and income tax thresholds frozen for additional three years beyond 2028

- Tax on property and savings income to rise by two percentage points for each tax band. Tax on dividend income to rise two percentage points for basic rate and higher rate taxpayers but not additional rate taxpayers

- Amount people can sacrifice from their salary to avoid paying NI on pension contributions capped at £2,000 a year from 2029

- Amount under-65s can put into cash ISAs capped at £12,000 a year, with the rest of the £20,000 annual allowance reserved for investments

- In England, properties worth more than £2 million face a £2,500 annual charge, rising to £7,500 for properties worth more than £5 million

- Cap limiting households on universal or child tax credit from receiving payments for a third or subsequent child to be scrapped from April

- By maintaining the triple lock policy, the basic and new state pension payments will go up by 4.8% from April, more than the current rate of inflation

- Three-year exemption for stamp duty reserve tax for companies that choose to list in the UK

- To protect high street retailers, there will be a new custom duty on deliveries from online businesses

- Defence spending to reach of 2.6% of GDP by 2027

What’s next?

For Hetal it will be important to dig into the numbers behind the Chancellor’s speech. Neither the tax increases nor the spending were particularly aggressive and the fiscal hole has been closed. Hetal retains a watchful eye on UK productivity and how it translates to growth and in the near term to the Bank of England’s interest rate policy.

The initial response from the gilt market, after the pre-announcement lurch in yields when the OBR report was accidently published too early, was somewhat muted, she notes.

|

*What is fiscal “headroom” and why does it matter? There are some self-imposed constraints the UK government uses to ensure responsible budgeting and sustainable public finances. These are known as fiscal rules. They are intended to maintain economic stability. The amount of flexibility the government has to increase spending, cut taxes or absorb a higher borrowing need without breaking these rules is what they call “headroom”. The Office for Budget Responsibility (OBR) then assesses whether the government is on track to stay within this buffer. If it cites concern over the levels, it can potentially lead to governments needing to act such as cut spending or raise taxes. This can create uncertainty and market volatility. Since 2010, UK chancellors have set aside on average £26 billion for this headroom. But it has been shrinking steadily for the past few years. SJP’s chief economist Hetal Mehta points out at the Conservatives’ last Spring Budget in 2024, remaining headroom was slim at £9.9 billion. At Labour’s first Budget in 14 years, Chancellor Rachel Reeves redefined some of the fiscal rules but maintained the headroom of £9.9 billion. However, by the Spring 2025 statement, the UK’s growth outlook had weakened, and the fiscal position had deteriorated by £14 billion. |

With these announcements adding yet more complexity to financial matters, the importance – and value – of financial advice has never been as clear. Find a financial adviser today.

The levels and bases of taxation and reliefs from taxation can change at any time. Tax relief is dependent on individual circumstances.

Most popular articles

Most recent articles